1. The Eighth Wonder of the World

There is a quote, widely attributed to Albert Einstein, that floats around every introductory finance seminar and wealth management seminar in the world: “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.” Whether or not the legendary physicist actually uttered those exact words is a matter of historical debate. However, the absolute truth behind the statement is undeniable.

When you place money into a savings account, buy a bond, or invest in the stock market, you expect to be compensated for the risk and the time your money is tied up. This compensation is called interest. But not all interest is created equal. There is a fundamental difference between earning a flat rate on your initial deposit and triggering a mathematical snowball effect. Understanding exactly why earning ‘interest on interest’ is called compound interest is the very first step to mastering personal finance and corporate wealth generation.

2. Etymology: What Does “Compound” Actually Mean?

To understand the financial concept, we must first look at the linguistic roots of the word itself. The word “compound” originates from the Latin word componere, which literally translates to “to put together” or “to combine” (from com- meaning ‘together’ and ponere meaning ‘to put’).

The Financial “Putting Together”

In the realm of finance, “compounding” refers to the specific action of taking the interest you just earned in a given period and putting it together with your original principal. This new, combined total becomes the base amount for calculating the next period’s interest.

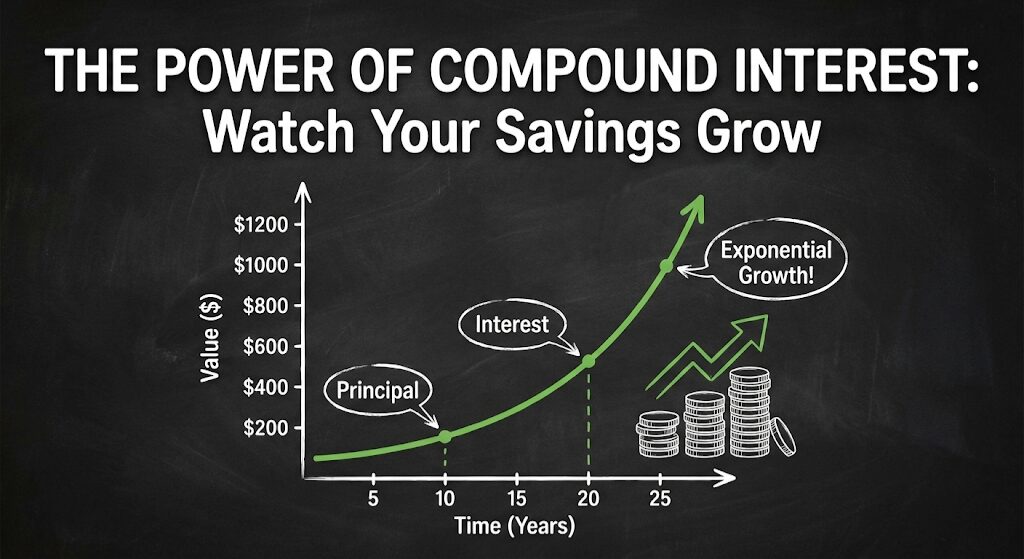

You are not keeping your principal and your interest separated in two different mental buckets. They are compounded into a single, larger entity. Because the base is now larger, the interest generated in the next cycle will also be larger. This process repeats, creating an accelerating, upward curve.

Calculate Your Future Wealth

Stop guessing how much your investments will be worth in 20 years. Equip yourself with a professional-grade Financial Calculator to instantly compute compound interest, NPV, and amortization schedules.

Browse Financial Calculators on Amazon3. The Core Mechanics: How “Interest on Interest” Works

The easiest way to grasp why this phenomenon is so powerful is to walk through a basic, step-by-step example.

Imagine you invest $10,000 in an account that pays a 10% annual interest rate.

- Year 1: You earn 10% on your initial $10,000. That equals $1,000. Your new account balance is $11,000.

- Year 2 (The Magic Happens): This is where compounding kicks in. You do not earn 10% on your original $10,000. You earn 10% on your new compounded principal of $11,000. Ten percent of $11,000 is $1,100. Your new balance is $12,100.

Notice that in Year 2, your interest payment was $100 higher than in Year 1. Where did that extra $100 come from? It came from the $1,000 in interest you earned in Year 1. Your interest earned its own interest. As the years go by, this effect magnifies. By Year 20, the vast majority of your annual growth is coming from interest-earning-interest, not from your original $10,000 deposit.

4. Simple Interest vs. Compound Interest

To truly appreciate compounding, it must be contrasted with its weaker cousin: Simple Interest. Simple interest is calculated only on the original principal amount, regardless of how much time passes or how much interest has accumulated.

| Year | Simple Interest (10% on $10k) | Compound Interest (10% on $10k) | The Difference |

|---|---|---|---|

| Year 1 | $11,000 (+$1,000) | $11,000 (+$1,000) | $0 |

| Year 5 | $15,000 (+$1,000/yr) | $16,105 | $1,105 |

| Year 10 | $20,000 (+$1,000/yr) | $25,937 | $5,937 |

| Year 30 | $40,000 (+$1,000/yr) | $174,494 | $134,494 |

As the table and graph demonstrate, simple interest represents a straight, linear line. Compound interest represents a parabolic, exponential curve. Over a 30-year horizon, the “interest on interest” effect results in a portfolio that is more than four times larger than the simple interest portfolio.

5. The Mathematical Formula Behind the Magic

While the concept is intuitive, accountants and financial software use specific algebraic formulas to calculate exact future values. The standard formula for compound interest is:

Let’s break down these variables:

- A (Amount): The final future value of the investment, including both the principal and all accumulated interest.

- P (Principal): The initial amount of money deposited or borrowed.

- r (Rate): The annual interest rate, expressed as a decimal (e.g., 8% = 0.08).

- n (Number): The number of times that interest is compounded per year (e.g., 12 for monthly, 1 for annually).

- t (Time): The total time the money is invested or borrowed, measured in years.

Transform Your Financial Future

Understanding the math is just the beginning. Discover the best-selling personal finance and investing books that teach you how to apply compounding to build lasting, generational wealth.

Shop Top Investing Books6. The Unrivaled Power of Time

If you look closely at the formula above, you will notice that time ($t$) is in the exponent. This is the most crucial takeaway for any investor: Time is the ultimate multiplier in wealth creation. Because time is an exponential factor, starting early is infinitely more powerful than starting later with more money.

The Tale of Two Investors

Consider Alice and Bob. Alice invests $5,000 a year from age 25 to 35, then stops completely. She invested $50,000 total. Her money compounds at 8% until she is 65.

Bob waits until age 35 to start. He invests $5,000 a year from age 35 to 65. He invested $150,000 total. His money also compounds at 8%.

At age 65, Bob has roughly $566,000. Alice, who invested three times LESS money but gave it 10 extra years to compound, has over $787,000. Time beats capital.

7. The Impact of Compounding Frequencies

Not all compounding schedules are the same. The variable $n$ in our formula dictates how often the bank (or the market) calculates your interest and adds it to your principal. Common frequencies include:

- Annually: Compounded once per year ($n=1$).

- Semi-Annually: Compounded twice per year ($n=2$). Common for bonds.

- Monthly: Compounded 12 times per year ($n=12$). Common for savings accounts and mortgages.

- Daily: Compounded 365 times per year ($n=365$). Common for credit cards.

The more frequently your money compounds, the faster it grows. This is because the “putting together” of principal and interest happens more often, allowing the new interest to start generating its own interest sooner. A 5% rate compounded daily will yield slightly more than a 5% rate compounded annually. This is known as the Annual Percentage Yield (APY).

8. Real-World Applications: Investing and Corporate Strategy

In the real world, compounding isn’t just about bank accounts; it is the fundamental driver of the global stock market. When you buy shares in a company, you are buying a slice of their future profits. When a company earns a profit, it can either pay it out as a dividend, or reinvest it into the business to grow faster.

This reinvestment is corporate compounding. In fact, when executives look at long-term growth, they often realize the financial and nonfinancial benefits of a firm engaging in strategic planning include leveraging compound growth through retained earnings. By systematically reinvesting profits into R&D, new factories, or marketing, the company grows exponentially, which is reflected in an exponentially rising stock price over decades.

9. The Dark Side: The Nightmare of Compounding Debt

Compound interest is entirely agnostic. It does not care if you are earning it, or if you owe it. While it is the greatest tool for building wealth, it is also the most vicious trap for debtors.

Credit card companies rely heavily on daily compounding. If you carry a balance of $5,000 on a credit card with a 24% Annual Percentage Rate (APR), the bank calculates your interest daily and adds it to your balance. The next day, you are paying interest on yesterday’s interest. This is exactly why the function of a financial manager heavily revolves around optimizing a company’s capital structure to avoid falling into high-interest compounding debt traps.

Build Your Own Financial Models

Learn how to model compound interest, track your investments, and build debt-payoff calculators. Grab a comprehensive guide to Microsoft Excel and take absolute control of your financial data.

Shop Excel Mastery Books10. Corporate Finance & Working Capital

For a business to survive long enough to reap the rewards of compound growth, it must manage its short-term liquidity. To ensure day-to-day operations run smoothly without dipping into expensive, high-interest short-term debt, a solid grasp of the concepts of working capital is mandatory.

Financial managers constantly monitor the difference between gross working capital (total current assets) and net working capital. If a company fails to manage this, they are forced to take on short-term loans. The compound interest on these emergency loans eats directly into the firm’s profit margins, destroying shareholder value.

11. The Rule of 72: A Mental Math Shortcut

If you don’t have a financial calculator handy, there is a brilliant mathematical shortcut to estimate the power of compounding: The Rule of 72.

This rule tells you roughly how many years it will take for an investment to double in value given a fixed annual rate of interest. You simply divide the number 72 by your expected annual interest rate.

- If you earn a 4% return: 72 ÷ 4 = 18 years to double.

- If you earn an 8% return: 72 ÷ 8 = 9 years to double.

- If you are paying 18% on a credit card: 72 ÷ 18 = 4 years for your debt to double.

This simple formula perfectly illustrates why hunting for a slightly higher yield (e.g., an S&P 500 index fund vs. a basic savings account) has catastrophic differences over a 30-year timeframe.

12. Pros and Cons of Compound Interest Systems

The Advantages

- Passive Wealth Generation: It allows money to work for you, requiring no physical labor to generate income.

- Inflation Protection: Compounding investments (like equities) are one of the only ways to outpace the eroding effects of inflation.

- Rewards Patience: It levels the playing field, allowing young people with small amounts of capital to become wealthy simply by waiting.

The Disadvantages

- The Debt Trap: It is merciless to borrowers. It can quickly cause consumer debt to spiral out of control.

- Requires Discipline: Compounding takes decades to show its true power. Human psychology struggles with delayed gratification.

- Inflation Erosion: If your compound interest rate (e.g., 1% in a bank) is lower than inflation (e.g., 3%), your real wealth is actually compounding negatively.

13. Conclusion: Harnessing the Mathematical Snowball

Understanding why earning ‘interest on interest’ is called compound interest is the dividing line between those who spend their lives working for money, and those whose money works for them. By “putting together” your principal and your earnings, you trigger a mathematical snowball effect that defies linear human logic.

The rules of the game are simple: start as early as possible, hunt for reasonable rates of return, let time do the heavy lifting, and absolutely avoid being on the paying end of compounding debt. Master these principles, and financial independence becomes not just a possibility, but a mathematical certainty.

Explore More Financial Concepts at Edmics