1. Introduction to Working Capital and Corporate Survival

In the brutal arena of corporate finance, profitability is an illusion if a company cannot pay its bills today. A firm can have millions of dollars in highly profitable sales on its income statement, yet still be forced into bankruptcy if it lacks the cash to pay its employees, suppliers, and short-term creditors. The lifeline that prevents this catastrophic collapse is known as working capital.

However, when executives and investors discuss this vital lifeline, they often use terms interchangeably, leading to dangerous financial misunderstandings. To accurately assess the short-term financial health of an enterprise, one must clearly define the difference between gross working capital and net working capital. While both metrics deal with the short-term assets of a business, they answer two fundamentally different questions about operational efficiency and solvency.

In this exhaustive guide, we will dissect both concepts, provide real-world balance sheet examples, analyze the strategic implications of liquidity management, and explain exactly why understanding these metrics is the hallmark of top-tier financial leadership.

2. What is Gross Working Capital (GWC)?

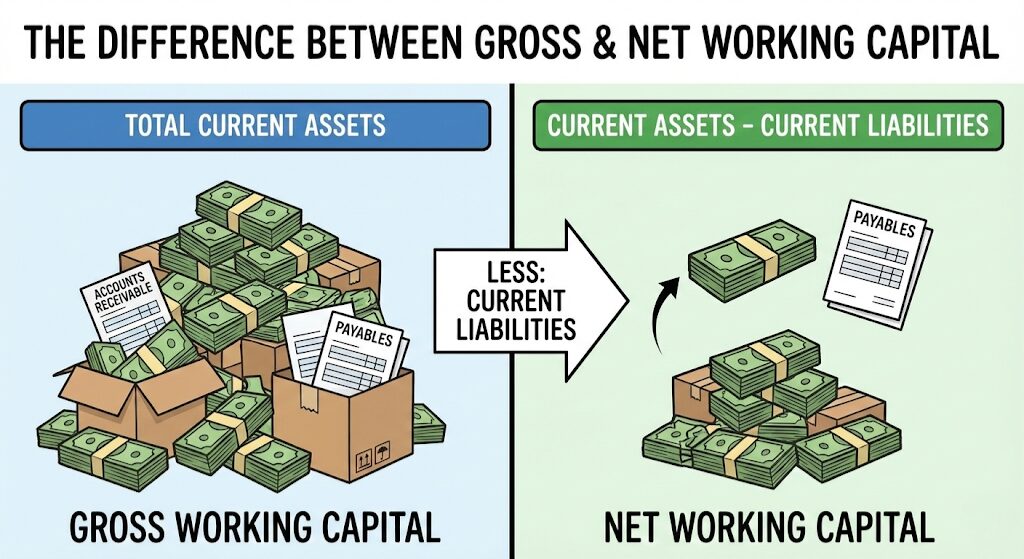

Gross Working Capital (GWC) is a strictly quantitative concept. It represents the total sum of all a company’s current assets. It does not factor in what the company owes; it simply looks at the total volume of funds tied up in the short-term operations of the business.

To fully grasp GWC, we must break down the specific components of concepts of working capital that make up current assets. These are resources expected to be converted into cash, sold, or consumed within a single operating cycle or one year:

- Cash and Cash Equivalents: Hard currency in bank accounts, petty cash, and highly liquid treasury bills.

- Marketable Securities: Short-term investments like commercial paper that can be liquidated in a matter of days.

- Accounts Receivable (AR): Money owed to the company by customers who purchased goods on credit.

- Inventory: Raw materials, work-in-progress (WIP), and finished goods waiting to be sold.

- Prepaid Expenses: Payments made in advance for goods or services to be received in the near future (e.g., prepaid insurance or rent).

The Purpose of Gross Working Capital

Why do we track GWC? It tells management the absolute scale of the company’s operational investment. If a company has a massive GWC, it means a vast amount of its capital is locked up in daily operations rather than long-term, yield-generating fixed assets. Optimizing the individual components of GWC is crucial for operational efficiency.

Master Corporate Accounting

Stop guessing at balance sheets. Equip yourself with a top-rated Financial Accounting and Corporate Finance textbook to deeply understand liquidity, solvency, and asset optimization.

Browse Accounting Textbooks3. What is Net Working Capital (NWC)?

While GWC tells you how much short-term capital the business holds, Net Working Capital (NWC) is a qualitative concept. It measures the true liquidity and short-term solvency of the firm by subtracting what the company owes in the short term from what it owns in the short term.

Current liabilities are obligations that the company must settle within one year or one operating cycle. They act as an immediate drain on the firm’s current assets. Key components include:

- Accounts Payable (AP): Money the company owes to its suppliers for raw materials or services purchased on credit.

- Short-Term Debt: Bank loans or lines of credit that are due within 12 months.

- Accrued Expenses: Expenses incurred but not yet paid (e.g., accrued wages, accrued taxes).

- Current Portion of Long-Term Debt: The fraction of a multi-year loan that must be paid off this year.

NWC provides a snapshot of financial health. If NWC is a positive number, the company has enough liquid assets to pay off all its immediate debts and still have a cushion to fund daily operations. If NWC is negative, the company is in a precarious position and may face insolvency.

4. Core Differences: Gross vs. Net Working Capital

To solidify the difference between gross working capital and net working capital, let’s look at a direct, side-by-side comparison of how these metrics are utilized by stakeholders.

| Feature | Gross Working Capital (GWC) | Net Working Capital (NWC) |

|---|---|---|

| Concept Type | Quantitative (Focuses on total volume/amount). | Qualitative (Focuses on financial health and liquidity). |

| Formula | Sum of all Current Assets. | Current Assets minus Current Liabilities. |

| Negative Values | Cannot be negative. The lowest possible value is zero. | Can be negative (if liabilities exceed assets). |

| Primary User | Operations managers analyzing inventory and receivables. | Creditors, banks, and investors evaluating solvency risk. |

| Indication of True Wealth | Poor indicator. A firm with high GWC might be drowning in short-term debt. | Strong indicator. Shows the true “cushion” a business has to survive shocks. |

5. The Operating Cycle and Cash Conversion Cycle

You cannot discuss working capital without discussing the speed at which it moves. The Operating Cycle is the time it takes for a company to purchase raw materials, convert them into finished goods, sell those goods, and collect the cash from customers.

[Image of the cash conversion cycle diagram]A subset of this is the Cash Conversion Cycle (CCC), which measures the time between when a company pays cash to its suppliers and when it receives cash from its customers. The formula is:

A lower CCC means the company’s capital is tied up for less time, increasing liquidity and reducing the need for external financing. If a company can stretch its DPO (pay suppliers later) while shrinking its DSO (collect from customers faster), it drastically improves its Net Working Capital position.

6. Real-World Calculation Example: TechFlow Inc.

Let’s look at a fictional balance sheet for a mid-sized hardware manufacturer, TechFlow Inc., to calculate both metrics.

TechFlow Inc. Balance Sheet Snapshot

Current Assets:

- Cash: $150,000

- Accounts Receivable: $200,000

- Inventory: $350,000

Total Current Assets: $700,000

Current Liabilities:

- Accounts Payable: $180,000

- Short-Term Bank Loan: $120,000

- Accrued Wages: $50,000

Total Current Liabilities: $350,000

1. Gross Working Capital Calculation:

GWC is simply the total current assets. Therefore, TechFlow’s GWC is $700,000. This tells the operations team they have $700k tied up in the short-term cycle.

2. Net Working Capital Calculation:

NWC = Current Assets ($700,000) – Current Liabilities ($350,000). TechFlow’s NWC is $350,000. This is a highly positive NWC. A bank looking at this business would be very comfortable issuing a loan, knowing the company has a massive $350k cushion to cover immediate obligations.

Calculate Financial Health Instantly

From determining Net Working Capital ratios to calculating compound growth and IRR, a professional financial calculator is the ultimate tool for corporate controllers and investors.

View Financial Calculators7. The Role of the Financial Manager in Capital Optimization

Working capital does not manage itself. In fact, optimizing these metrics is one of the primary duties of the corporate finance department. Understanding the function of a financial manager is key to seeing how these numbers move on a day-to-day basis.

A financial manager is constantly walking a tightrope between liquidity and profitability. If they keep too much cash on hand (high NWC), the company is safe, but that cash is sitting idle, earning no return. If they invest all the cash into long-term assets to boost profitability (low NWC), the company might miss payroll next week.

The manager must implement aggressive strategies: negotiating strict payment terms with slow-paying clients to reduce Accounts Receivable, utilizing Just-In-Time (JIT) inventory systems to reduce gross working capital tied up in warehouses, and securing favorable short-term credit facilities to bridge temporary cash flow gaps.

8. Positive vs. Negative Net Working Capital

While positive NWC is the standard goal for most businesses, the financial landscape is filled with nuances. The industry a company operates in heavily dictates what an “acceptable” NWC looks like.

Positive NWC: The Safety Net

A positive NWC means the company can comfortably pay its short-term debts. However, if the NWC is too positive (e.g., a current ratio of 4:1), it signals inefficiency. The company is hoarding cash or allowing inventory to bloat rather than investing in growth or paying dividends to shareholders.

Negative NWC: Bankruptcy Risk or Strategic Masterstroke?

Generally, negative NWC is a massive red flag indicating an impending liquidity crisis. The company owes more than it has readily available. However, there are fascinating exceptions. Massive retail giants like Walmart or Amazon often operate with negative NWC. Why?

Because their inventory turnover is incredibly fast. They sell inventory to customers for cash within days, but they have negotiated terms with their suppliers to pay their Accounts Payable in 60 or 90 days. They collect cash long before they have to pay their bills, allowing them to use their suppliers’ money to fund their operations.

9. Investing Surplus Capital: The Power of Yield

When a financial manager successfully optimizes the company’s gross working capital and maintains a healthy, stable net working capital, a magical thing happens: the company generates surplus cash. What should be done with this excess liquidity?

It must be put to work. Leaving surplus cash in a checking account allows inflation to erode corporate purchasing power. By investing excess NWC into short-term, yield-bearing instruments (like Treasury bills or commercial paper), the company triggers exponential wealth generation. If you want to understand the mathematics behind this growth, you must understand why earning interest on interest is the most powerful force in finance. Compound interest turns stagnant, defensive cash reserves into an active, revenue-generating arm of the business.

10. Pros and Cons of Focusing on Each Metric

Both metrics have their place in financial analysis, but heavily favoring one over the other can lead to management blind spots.

Focusing on Gross Working Capital

- Pro: Excellent for operational managers who need to track inventory levels and sales team performance (AR).

- Pro: Highlights exactly where capital is physically tied up in the business process.

- Con: Highly deceptive to investors. A high GWC looks impressive but completely ignores the debt funding those assets.

Focusing on Net Working Capital

- Pro: The ultimate truth-teller regarding a company’s immediate survival and solvency risk.

- Pro: A preferred metric for banks and creditors when deciding to issue commercial loans.

- Con: Can encourage managers to hoard cash to make the balance sheet look “safe,” missing out on aggressive growth opportunities.

11. Long-Term Strategic Implications

Working capital is a short-term metric, but it is deeply intertwined with long-term corporate destiny. A company cannot execute a bold, 5-year strategic vision if it is constantly worried about covering next week’s payroll.

This is where executive leadership steps in. When forecasting capital requirements, executives rely on the financial and nonfinancial benefits of a firm engaging in strategic planning. A robust strategic plan will forecast future NWC requirements. For example, if the strategy is to double sales next year, the company will need massive amounts of Gross Working Capital to buy inventory upfront. By predicting this need, the firm can secure a line of credit months in advance, rather than facing a cash crunch during rapid expansion.

Build a Bulletproof Corporate Strategy

Combine your working capital management with long-term vision. Explore top-rated business strategy and corporate planning books to guarantee your company thrives in competitive markets.

Explore Business Strategy Books12. Conclusion: The Dual Pillars of Liquidity

Understanding the difference between gross working capital and net working capital is the dividing line between amateur bookkeeping and professional financial management. Gross Working Capital (the sum of current assets) provides the sheer volume of resources moving through the operational cycle, acting as the fuel for daily business activities.

Conversely, Net Working Capital (current assets minus current liabilities) reveals the underlying strength of the engine. It strips away the debt to show the true, unencumbered liquidity of the firm. By monitoring, managing, and optimizing both of these metrics simultaneously, financial leaders can ensure their companies survive short-term shocks and thrive in long-term markets.

Explore More Financial Concepts at Edmics