Fidelity vs Charles Schwab: The Ultimate Side-by-Side Breakdown

Which brokerage wins on fees, tools, retirement accounts, research, and overall value for investors in 2026?

Overview: Two Giants Compared

⚡ Last verified: March 2026If you’ve been searching for the best full-service brokerage, you’ve almost certainly landed on one of two names: Fidelity Investments and Charles Schwab. Both are powerhouses that have shaped American investing for decades. Fidelity, founded in 1946, manages over $14 trillion in assets. Schwab, founded in 1971 and now bolstered by its 2020 acquisition of TD Ameritrade, oversees more than $9 trillion in client assets.

These aren’t fringe competitors — they’re the two most recommended brokerages for everyday investors, retirees, and even sophisticated traders. The problem is that choosing between them isn’t obvious. Both offer commission-free stock trading, a wide range of account types, extensive research, and solid mobile apps. So what really separates them?

This comparison digs into every layer — from fee structures and trading tools to retirement-specific features and customer service quality — so you can make the right call for your financial goals. Whether you’re just starting your investing journey or you’re a seasoned portfolio manager hunting for the best platform, this guide will give you the full picture.

At a Glance: Key Stats

| Feature | Fidelity | Charles Schwab |

|---|---|---|

| Founded | 1946 | 1971 |

| AUM | ~$14 trillion | ~$9.4 trillion |

| Stock commissions | $0 | $0 |

| Options (per contract) | $0.65 | $0.65 |

| Account minimum | $0 | $0 |

| FDIC-insured cash | Up to $5M (via program banks) | Up to $500K |

| Branch locations | ~200 | ~400 |

| Robo-advisor | Fidelity Go | Schwab Intelligent Portfolios |

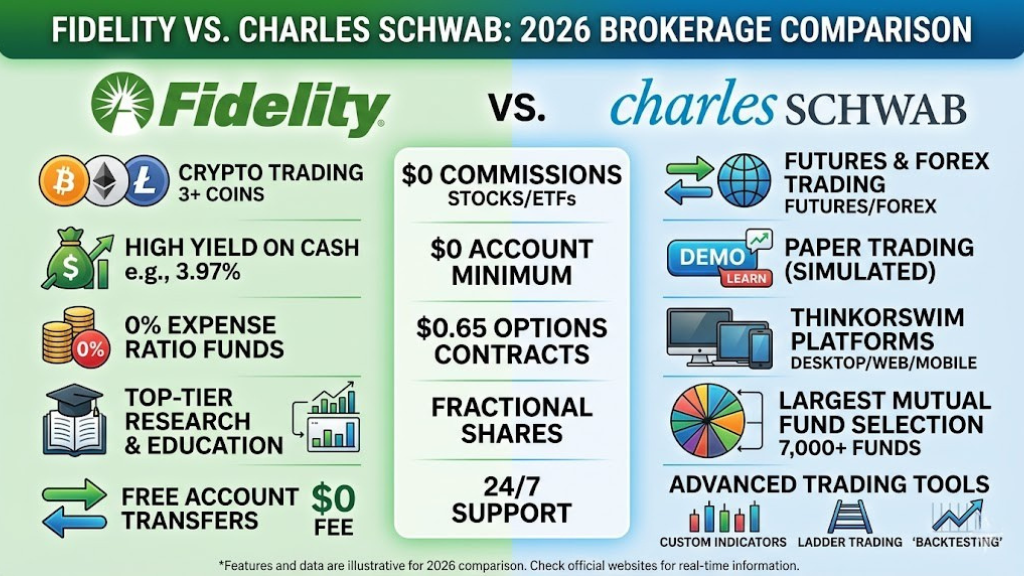

Fees & Commissions

The fee war between major brokerages has largely been won — by investors. Both Fidelity and Schwab eliminated stock trading commissions in 2019, following a race-to-the-bottom that disrupted the entire industry. But commissions are just one piece of the cost puzzle. Where they differ is in the finer details: options fees, mutual fund fees, margin rates, and — critically — expense ratios on their proprietary funds.

Stock & ETF Trading

Both platforms charge $0 per trade for US stocks and ETFs listed on major exchanges. This parity extends to fractional shares, which both platforms support, allowing investors to buy partial shares of high-priced stocks like Amazon or Berkshire Hathaway.

Options Trading

Both charge $0.65 per contract for options, with no base commission. This is industry-standard pricing. Neither platform offers the reduced $0.50/contract that platforms like tastytrade advertise, but for most retail investors, the research tools and platform stability justify the cost.

Mutual Funds

This is where a meaningful gap opens. Fidelity has zero-expense-ratio index funds — literally funds that cost you nothing to hold annually. Fidelity ZERO Total Market Index Fund (FZROX) and Fidelity ZERO International Index Fund (FZILX) have 0.00% expense ratios. Schwab’s equivalent index funds are low — around 0.03% — but they’re not zero.

Margin Rates

Margin rates fluctuate, but historically Schwab has offered slightly more competitive rates for larger margin balances. Fidelity’s margin rates are competitive for smaller balances. For most retail investors not using margin regularly, this distinction matters little.

Cost Comparison at a Glance

📚 Recommended: The Little Book of Common Sense Investing

John Bogle’s definitive guide to low-cost index fund investing — perfect for Fidelity ZERO fund users.

View on Amazon →Account Types Available

One of the strongest selling points of both Fidelity and Schwab is their breadth of account offerings. Whether you need a simple brokerage account, a tax-advantaged retirement vehicle, a custodial account for your kids, or a trust account for estate planning, both platforms have you covered.

| Account Type | Fidelity | Schwab |

|---|---|---|

| Individual Brokerage | ✔ | ✔ |

| Joint Brokerage | ✔ | ✔ |

| Traditional IRA | ✔ | ✔ |

| Roth IRA | ✔ | ✔ |

| SEP-IRA | ✔ | ✔ |

| SIMPLE IRA | ✔ | ✔ |

| Solo 401(k) | ✔ | ✔ |

| 529 College Savings | ✔ | ✘ (via 3rd party) |

| HSA | ✔ | ✘ |

| Custodial (UGMA/UTMA) | ✔ | ✔ |

| Trust Account | ✔ | ✔ |

| Cash Management Account | ✔ | ✔ |

The standout differentiator here is Fidelity’s native Health Savings Account (HSA) offering. HSAs are one of the most powerful tax-advantaged accounts available — contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. If you’re exploring comprehensive wealth management strategies, incorporating an HSA alongside your retirement accounts is a move Fidelity makes particularly seamless.

Fidelity also offers a direct 529 plan with competitive options and solid investment choices. Schwab directs customers to third-party 529 providers instead, which adds friction to the process.

Investment Options

The range of what you can invest in is critical — particularly as portfolios grow more sophisticated. Both Fidelity and Schwab offer an enormous universe of options, but the composition differs in ways that matter for different investor types.

Stocks & ETFs

Both brokers provide access to virtually all NYSE, NASDAQ, and AMEX-listed securities. Schwab’s acquisition of TD Ameritrade also brought in thinkorswim, which gives Schwab users access to one of the most powerful active-trading environments available anywhere. For long-term buy-and-hold ETF investors — particularly those building portfolios around top dividend-paying stocks — both platforms perform equally well.

Mutual Funds

Fidelity has over 10,000 mutual funds available, including its own family with zero-expense-ratio options. Schwab offers around 4,000+ no-transaction-fee mutual funds. Fidelity’s edge here is its proprietary fund quality and cost structure.

Bonds & Fixed Income

Both platforms offer access to corporate bonds, municipal bonds, Treasury securities, CDs, and bond funds. Schwab’s fixed-income research and bond ladder tools have historically been praised by retirement-focused investors.

Options

Both support full options trading, from basic covered calls to complex multi-leg strategies. Schwab’s thinkorswim platform pulls ahead here for sophisticated options traders who need advanced analytics and paper trading capabilities.

Crypto

As of 2026, neither Fidelity nor Schwab offers direct cryptocurrency trading through their standard brokerage platforms. However, both offer exposure through Bitcoin ETFs and crypto-related funds. Fidelity has expanded its institutional crypto offerings, though retail access remains primarily through fund vehicles. For direct crypto investing, you may want to explore a hardware wallet for secure self-custody.

International Investing

Both offer international stock trading, though the ease and fee structure differs. Fidelity charges lower commissions on international trades and provides more direct access to foreign markets, making it a better choice for globally diversified portfolios.

Investment Universe Comparison

📖 Recommended: A Random Walk Down Wall Street

Burton Malkiel’s classic on passive investing strategy — a must-read for index fund investors at both Fidelity and Schwab.

View on Amazon →Trading Platforms & Tools

This is arguably the biggest differentiator between Fidelity and Schwab for active investors. When Schwab acquired TD Ameritrade in 2020, it inherited thinkorswim — widely regarded as the most powerful retail trading platform ever built. Fidelity counters with Active Trader Pro, which is robust but occupies a different tier of sophistication.

Fidelity Active Trader Pro

Active Trader Pro is a downloadable desktop application with customizable layouts, streaming real-time quotes, Level II data, and a full suite of technical indicators. It’s excellent for intermediate to advanced investors — but it lacks some of the professional-grade features that thinkorswim offers.

Schwab thinkorswim

thinkorswim is the crown jewel of Schwab’s platform offering. It supports thinkScript (a proprietary scripting language for custom indicators), paper trading (allowing practice with real market data without real money), advanced options analytics, economic data integration, and one of the best charting engines available at any price point. For serious active traders, there’s simply nothing like it in the retail space.

Web Platforms

Both offer competitive web-based platforms. Fidelity’s web experience is cleaner and more intuitive for casual investors. Schwab.com integrates well with the broader Schwab ecosystem including bank accounts and advisory tools.

Platform Comparison Widget

Research & Education

For investors who want to make data-driven decisions — or who are still learning the ropes — the quality and depth of research tools is paramount. Both Fidelity and Schwab offer substantial resources, but with different emphases.

Fidelity’s Research Ecosystem

Fidelity provides research from over 20 independent providers, including Zacks, Argus, Value Line, and Morningstar. Their stock screeners are among the most powerful available for retail investors, with more than 140 customizable criteria. Fidelity’s Learning Center offers thousands of articles, videos, webinars, and courses ranging from beginner budgeting fundamentals to advanced options strategies.

Fidelity’s Equity Summary Score aggregates analyst ratings into a single 1-10 score, giving investors a quick, data-backed read on any individual stock.

Schwab’s Research Ecosystem

Schwab offers research from Morningstar, Credit Suisse, and its own Schwab Equity Ratings. Their Market Edge tool provides technical analysis ratings. The Schwab Learning Center and the Insights & Ideas section feature regular market commentary from their own Chief Investment Strategist, which many investors find genuinely useful for macro context.

Schwab’s acquisition of TD Ameritrade also brought in premium research tools previously available only to TD clients, further strengthening its offering.

Education Comparison: Flip Card Pros & Cons

Hover (desktop) or tap (mobile) each card to reveal details.

Retirement Features

Retirement planning is where the stakes are highest for most investors, and both Fidelity and Schwab take it seriously. If you’re thinking about how much you should be saving for retirement, both platforms offer excellent calculators, planning tools, and account options to support those goals.

Retirement Account Breadth

Both platforms support the full spectrum of retirement account types: Traditional IRA, Roth IRA, SEP-IRA, SIMPLE IRA, and Solo 401(k). Fidelity additionally offers the HSA, which functions as a triple-tax-advantaged retirement health savings vehicle. For self-employed individuals and small business owners, both offer competitive Solo 401(k) plans with Roth contribution options.

Rollover Services

Rolling over a 401(k) from a former employer is a common but potentially confusing process. Fidelity’s rollover concierge service is highly rated — they’ll handle much of the paperwork and even call your previous plan provider on your behalf. Schwab also offers rollover support, but Fidelity’s guided service is generally considered smoother.

Robo-Advisors

Fidelity’s Fidelity Go is a clean, low-cost robo-advisor with no advisory fee for balances under $25,000 and 0.35% annually for larger accounts. It invests exclusively in Fidelity Flex mutual funds with no underlying fund fees, making it genuinely low-cost.

Schwab’s Intelligent Portfolios charges no advisory fee — but it requires a minimum cash allocation (around 6-10%) that sits in Schwab’s own money market products, which critics argue represents a hidden cost. Schwab Intelligent Portfolios Premium adds unlimited CFP access for $30/month.

Retirement Score Meters

🏖 Recommended: Retire Before Mom and Dad

Rob Berger’s practical guide to financial independence and early retirement — works beautifully with either Fidelity or Schwab accounts.

View on Amazon →Mobile App Experience

In an era where many investors manage their portfolios entirely from smartphones, the quality of a broker’s mobile app has become a major decision factor. Both Fidelity and Schwab have invested heavily in their mobile experiences — but they cater to slightly different users.

Fidelity Mobile App

Fidelity’s mobile app is consistently rated among the best in the industry on both the App Store (typically 4.8/5) and Google Play (4.5+). The design is clean and highly intuitive — it’s particularly well-suited for investors who want to check balances, execute trades, review research, and manage retirement accounts in a seamless, frictionless experience. Features include mobile check deposit, bill pay, instant transfers, and full account management for all Fidelity accounts including HSA and 529.

Schwab Mobile App

Schwab’s primary mobile app is solid and well-designed, earning high ratings (4.8 on App Store, 4.3+ on Google Play). It handles standard account management, trading, and banking functions well. The standout mobile offering from Schwab, however, is the thinkorswim mobile app — a separate application that brings most of the desktop platform’s power to your phone, including advanced charting, options analysis, and paper trading. For active traders who want professional tools on mobile, this is exceptional.

Mobile App Feature Accordion

- Best-in-class UI simplicity rated consistently 4.8/5 on App Store

- Full HSA, 529, and retirement account management from mobile

- Mobile check deposit and Fidelity Cash Management features

- Biometric login, fraud alerts, and strong security protocols

- Research and Equity Summary Score available on mobile

- Fractional shares purchasing directly from the app

- Two apps: Schwab Mobile for everyday use + thinkorswim for advanced trading

- thinkorswim mobile offers professional-grade charting and options tools

- Paper trading available on thinkorswim mobile

- Integrated banking: check deposit, bill pay, ATM access

- Schwab Satisfaction Guarantee visible within the app

- Real-time streaming quotes and customizable watchlists

Choose Fidelity if: you want a single, unified app that covers all your financial life simply and elegantly. It’s best for retirement savers, ETF investors, and anyone who values simplicity and speed.

Choose Schwab (thinkorswim) if: you trade frequently, use options extensively, or want paper trading to test strategies on the go. The power-user mobile experience is unmatched.

Banking & Cash Management

The lines between brokerage and banking have blurred significantly over the past decade. Both Fidelity and Schwab have evolved well beyond pure investment platforms, offering checking accounts, debit cards, ATM fee reimbursements, and competitive interest rates on uninvested cash.

Fidelity Cash Management Account

Fidelity’s Cash Management Account (CMA) is one of the most compelling banking-adjacent products in the market. Key features include:

- Unlimited ATM fee reimbursements worldwide — Fidelity covers any ATM fee you’re charged, anywhere

- FDIC insurance up to $5 million through a network of program banks

- Competitive yield on cash through the Fidelity Government Money Market Fund

- No monthly fees, no minimum balance

- Bill pay and mobile check deposit

- Fidelity Visa debit card with 2% cash back (via Elan Financial)

Schwab Bank High Yield Investor Checking

Schwab operates its own FDIC-insured bank — Charles Schwab Bank — providing a fully integrated checking experience. Key features include:

- Unlimited ATM fee reimbursements worldwide (matching Fidelity)

- FDIC insured up to $500,000 (standard limits)

- Competitive yield through Schwab Bank High Yield Investor Savings

- No fees, no minimums

- Seamless integration between brokerage and bank accounts

The key distinction is FDIC coverage: Fidelity’s $5 million coverage through program banks dwarfs Schwab’s standard $500,000 limit. For high-net-worth individuals with large cash positions, this is a material advantage. Both platforms offer excellent cash management overall — if you’re actively deciding where to invest or park your money, the cash management features of both are worth factoring into your decision.

Customer Service

Even the best technology breaks down, and when you have an urgent question about your retirement account or a trade execution issue, you need reliable human support. This is an area where Schwab and Fidelity both excel — but in different ways.

Fidelity Customer Service

Fidelity offers 24/7 phone support, live chat, and email. Their phone wait times are generally low, and their representatives are consistently praised for being knowledgeable about complex account issues, particularly retirement planning questions. Fidelity operates approximately 200 investor centers in major US cities for in-person consultations.

Schwab Customer Service

Schwab also provides 24/7 phone and chat support. Where Schwab significantly outpaces Fidelity is in its physical branch network. With over 400 branch locations across the country (expanded further through the TD Ameritrade integration), Schwab is the clear winner for investors who want face-to-face advisory support. Schwab’s branch advisors are CFP-certified in many locations, providing access to free financial planning consultations.

J.D. Power Rankings

Both firms consistently score at or near the top of J.D. Power investor satisfaction surveys. In recent years, Fidelity has edged ahead in overall customer satisfaction with self-directed investing, while Schwab scores highly in full-service and advisory client satisfaction.

Who Wins? Category-by-Category Breakdown

Interactive Filterable Comparison Table

| Category | Fidelity | Schwab | Winner |

|---|---|---|---|

| Fees & Commissions | $0 trades, 0% fund ERs | $0 trades, 0.03% fund ERs | Fidelity |

| Account Variety | IRA, HSA, 529, more | IRA, 401k, no native HSA | Fidelity |

| Investment Options | Stocks, ETFs, bonds, futures, options | Same + forex via thinkorswim | Tie |

| Trading Platform | Active Trader Pro | thinkorswim | Schwab |

| Research & Education | 20+ providers, excellent screeners | Good research, macro commentary | Fidelity |

| Retirement Tools | HSA, rollover concierge, Fidelity Go | Intelligent Portfolios, branch CFPs | Fidelity |

| Mobile App | Unified, intuitive, 4.8★ | Two apps, thinkorswim mobile | Tie |

| Banking / Cash Mgmt | $5M FDIC, 2% debit cashback | $500K FDIC, ATM reimbursement | Fidelity |

| Customer Service | 24/7, ~200 branches | 24/7, 400+ branches, CFP access | Schwab |

| Options Tools | Solid, standard | thinkorswim: industry-leading | Schwab |

| Robo-Advisor | Fidelity Go: transparent, low cost | Intelligent Portfolios: cash drag | Fidelity |

| Paper Trading | Not available | Yes (thinkorswim) | Schwab |

As the table above shows, Fidelity wins 6 categories, Schwab wins 4, and 2 are ties. But raw category wins don’t tell the whole story — the weight of each category depends entirely on your personal investing style and goals.

The Verdict: Which Should You Choose?

The honest answer is: both are excellent. You won’t make a catastrophic mistake choosing either one. But based on investor type, here’s a clear recommendation framework:

🟢 Choose Fidelity if you are a…

- Long-term index fund investor seeking the lowest possible costs

- Retirement saver who wants HSA + IRA + 529 in one place

- Beginner who wants an intuitive learning experience

- High-net-worth cash holder wanting $5M FDIC coverage

- Someone who wants no-fee rollover support for old 401(k)s

- Dividend income investor building a high-yield dividend portfolio

🔵 Choose Schwab if you are a…

- Active trader who needs thinkorswim’s advanced tools

- Options trader who wants paper trading and analytics

- Investor who values in-person branch access (400+ locations)

- Someone seeking free CFP financial planning in a branch

- Fixed-income investor who wants Schwab’s bond laddering tools

- Trader drawn to the premium thinkorswim mobile experience

If you’re just starting your investment journey and are exploring the full landscape of best investments for 2026, Fidelity’s combination of zero costs, excellent education, and comprehensive account types makes it the slightly stronger starting point for most investors.

Frequently Asked Questions

Conclusion: Making Your Final Choice

After a thorough analysis of every major dimension — fees, account types, investment options, trading platforms, research, retirement features, mobile experience, banking, and customer service — Fidelity emerges as the marginally stronger choice for most investors, particularly those focused on long-term wealth building and retirement.

Fidelity’s zero-expense-ratio index funds, native HSA, superior rollover support, and $5 million FDIC cash coverage create a genuinely unbeatable package for cost-conscious, long-term investors. Its educational platform and clean user experience make it the best entry point for beginners, while its depth of research tools scales well for experienced investors.

Schwab, however, isn’t a consolation prize — it’s an extraordinary platform. For active traders, options enthusiasts, or anyone who values in-person financial planning, Schwab’s combination of thinkorswim and 400+ branch locations is a compelling, distinctive offering that Fidelity genuinely can’t match.

The smartest strategy? Many experienced investors hold both — and as you grow your financial sophistication and expand your portfolio into areas like real estate investing and alternative assets, having accounts at multiple brokerages gives you flexibility, redundancy, and access to the best of each platform’s strengths.

📗 Recommended: The Intelligent Investor by Benjamin Graham

Warren Buffett’s favorite investing book. The timeless principles apply whether you invest through Fidelity, Schwab, or anywhere else.

View on Amazon →