1. Introduction: The Psychology of Money and Prioritization

For millions of people, the word “budget” triggers immediate feelings of anxiety, restriction, and financial claustrophobia. It feels like a diet for your wallet—a mechanism designed solely to prevent you from enjoying life. However, this perspective is entirely backward. A budget is not a cage; it is a blueprint for your freedom. As financial experts frequently say, a budget is simply telling your money where to go instead of wondering where it went.

The primary reason most people fail at budgeting isn’t a lack of math skills; it is a lack of prioritization. When faced with rent, credit card bills, a desire to invest, a broken car transmission, and the temptation of a weekend getaway, human psychology naturally defaults to panic or avoidance. Without a clear hierarchy of needs, money is squandered on immediate gratification while long-term security crumbles.

If you are wondering exactly what should be prioritized when creating a budget, you are in the right place. In this masterclass, we will construct a bulletproof financial hierarchy. By ordering your financial life through these specific, non-negotiable tiers, you will eliminate the anxiety of money management and pave a mathematical road to genuine wealth.

2. Step 1: Establishing the Baseline (Income vs. Expenses)

Before you can prioritize where your money is going, you must have an absolute, unvarnished understanding of reality. You cannot prioritize a budget based on guesses or “mental math.”

First, calculate your Total Net Income. This is your take-home pay—the exact amount of money that hits your bank account after taxes, health insurance premiums, and employer deductions are removed. If you have a variable income (freelance, commission-based), calculate your baseline using your lowest-earning month from the past year. This prevents you from over-projecting your resources.

Second, conduct a ruthless audit of your last three months of bank statements. Every single transaction must be categorized. This exercise almost always reveals shocking “money leaks”—hundreds of dollars bleeding out through forgotten subscriptions, excessive takeout, or impulse online shopping.

Take Immediate Control of Your Cash Flow

Writing down your expenses engages your brain differently than looking at a screen. Grab a premium physical Budget Planner to meticulously track your income, eliminate money leaks, and crush your financial goals.

Shop Budget Planners on Amazon3. Priority #1: The Four Walls (Survival)

The Absolute Necessities

When creating a budget—especially if your income is tight or you are facing a financial crisis—your absolute first priority is survival. Personal finance experts refer to this as protecting “The Four Walls.” Until these four categories are fully funded, not a single dollar should be directed anywhere else.

- 1. Food: This means basic groceries to keep you and your family fed. It absolutely does not include dining out, delivery apps, or expensive coffee shop runs.

- 2. Shelter: Your rent or mortgage payment. Keeping a roof over your head is non-negotiable.

- 3. Basic Utilities: Water, electricity, and heating/gas. (Note: A premium cable package or multiple streaming services do not count as basic utilities).

- 4. Essential Transportation: The fuel, basic maintenance, and public transit costs required to get you to and from your place of employment. If you cannot get to work, you cannot generate the income required to fund the budget.

If you are experiencing a severe financial hardship, you must pay for The Four Walls before you pay your credit card minimums, student loans, or medical bills. Protect your survival first.

4. Priority #2: The Emergency Fund (Your Financial Shield)

The Starter Emergency Fund

Once your Four Walls are secured, your immediate next priority is building a financial buffer between you and disaster. Life is wildly unpredictable. Tires blow out, HVAC systems fail, and medical emergencies happen. Without an emergency fund, these normal life events become debt-inducing catastrophes.

Your goal here is a Starter Emergency Fund of $1,000 to $2,000. This money should be kept in a highly liquid, easily accessible savings account. It is not an investment; it is insurance. By having this buffer, you ensure that when the alternator in your car breaks, you do not have to put the $800 repair on a credit card carrying a 24% interest rate.

Note: Once you complete Priority #3 (Debt Elimination), you will return to this tier to expand this starter fund into a fully-funded 3 to 6 months of living expenses.

5. Priority #3: High-Interest Debt Elimination (The Wealth Killer)

Stopping the Bleeding

If you have consumer debt, your budget is effectively leaking money. High-interest debt (like credit cards, personal loans, and payday loans) is mathematically designed to keep you broke. Your third budget priority is to attack this debt with terrifying intensity.

There are two primary psychological and mathematical frameworks for prioritizing debt payoff:

| Method | How It Works | Best For |

|---|---|---|

| The Debt Snowball | List debts from smallest balance to largest balance. Pay minimums on everything, but throw every extra dollar at the smallest balance until it is gone. Roll that payment into the next smallest. | People who need quick psychological “wins” to stay motivated. It changes behavior through momentum. |

| The Debt Avalanche | List debts from highest interest rate to lowest interest rate. Attack the highest interest rate first, regardless of the balance size. | People who are highly disciplined and want to mathematically pay the absolute least amount of interest over time. |

The 401(k) Match Exception

There is one massive exception to the “pay off all debt before investing” rule. If your employer offers a 401(k) match, you should prioritize contributing just enough to capture that match before attacking your debt. An employer match is a guaranteed 100% return on your investment. You will never beat a 100% return anywhere else.

Destroy Debt and Build Lasting Wealth

Need a proven roadmap? Discover the most highly-rated personal finance books that teach you the exact psychological and mathematical strategies needed to escape the paycheck-to-paycheck cycle forever.

Browse Top Finance Books6. Priority #4: Retirement and Long-Term Investing

Paying Your Future Self

With your Four Walls secured, your starter emergency fund in place, and your toxic high-interest consumer debt eliminated, your budget transitions from defense to offense. It is time to prioritize wealth generation.

The standard financial consensus is that you must prioritize saving 15% to 20% of your gross income for retirement. If you are wondering how much should I save for retirement, it depends entirely on your age and goals, but 15% is the universal baseline.

When directing this 15% through your budget, prioritize tax-advantaged accounts in this specific order:

- Max out the Employer Match: (If you haven’t already).

- Fund a Roth IRA: A Roth IRA allows your investments to grow completely tax-free, and you pay zero taxes when you withdraw the money in retirement.

- Max out a Health Savings Account (HSA): If you have a high-deductible health plan, an HSA offers a rare “triple-tax advantage” (tax-free contributions, tax-free growth, tax-free withdrawals for medical expenses).

- Return to the 401(k): If you still haven’t hit your 15% goal, funnel the remainder back into your traditional employer 401(k).

If you are looking to accelerate this phase, researching where to invest money outside of standard retirement accounts—such as broad-market index funds or real estate—is your next logical step.

7. Priority #5: Short-Term Savings Goals

Sinking Funds

Your budget must account for large expenses that you know are coming, but don’t happen every month. Prioritizing these goals prevents you from dipping into your emergency fund or going back into credit card debt.

You achieve this through “Sinking Funds.” You identify a future expense, determine when it is due, and divide the total cost by the number of months you have to save for it. This amount becomes a monthly priority in your budget.

- Examples of Sinking Funds: Annual property taxes, Christmas/holiday gifts, an upcoming family vacation, or a down payment for a replacement vehicle.

By treating your annual vacation like a monthly bill, the money is sitting in your account exactly when you need it.

8. Priority #6: Discretionary Spending (Guilt-Free Fun)

The Wants

Only after you have funded your survival, your emergency shield, your debt payoff, your future retirement, and your known upcoming expenses do you allocate money to your “Wants.”

This is where subscriptions, dining out, concert tickets, and new clothes live. Many people fail at budgeting because they place this tier at the top. They buy a new wardrobe, go out for drinks all weekend, and then try to invest whatever “is left over” at the end of the month. The harsh reality is that there is rarely anything left over.

By placing discretionary spending at the bottom of the priority list, you flip the script. You guarantee your financial security first. Then, whatever money drops down to this final tier can be spent 100% guilt-free, knowing your future is entirely secure.

Calculate Your Compound Growth

Ensure your retirement projections and debt payoff timelines are mathematically perfect. A professional financial calculator allows you to easily compute interest rates, amortization schedules, and future investment values.

View Financial Calculators9. Popular Budgeting Frameworks to Enforce Priorities

Knowing what to prioritize is the strategy. A budgeting framework is the tactical tool used to execute that strategy. Depending on your personality and financial discipline, integrating financial planning tips with a specific framework will yield the best results.

Zero-Based Budgeting (Highly Recommended)

In this framework, Income minus Expenses equals Zero. Every single dollar of your income is given a specific job before the month begins. If you have $200 left over after funding all priorities, you don’t leave it in checking; you assign it to an investment or debt category. It requires discipline but offers maximum control.

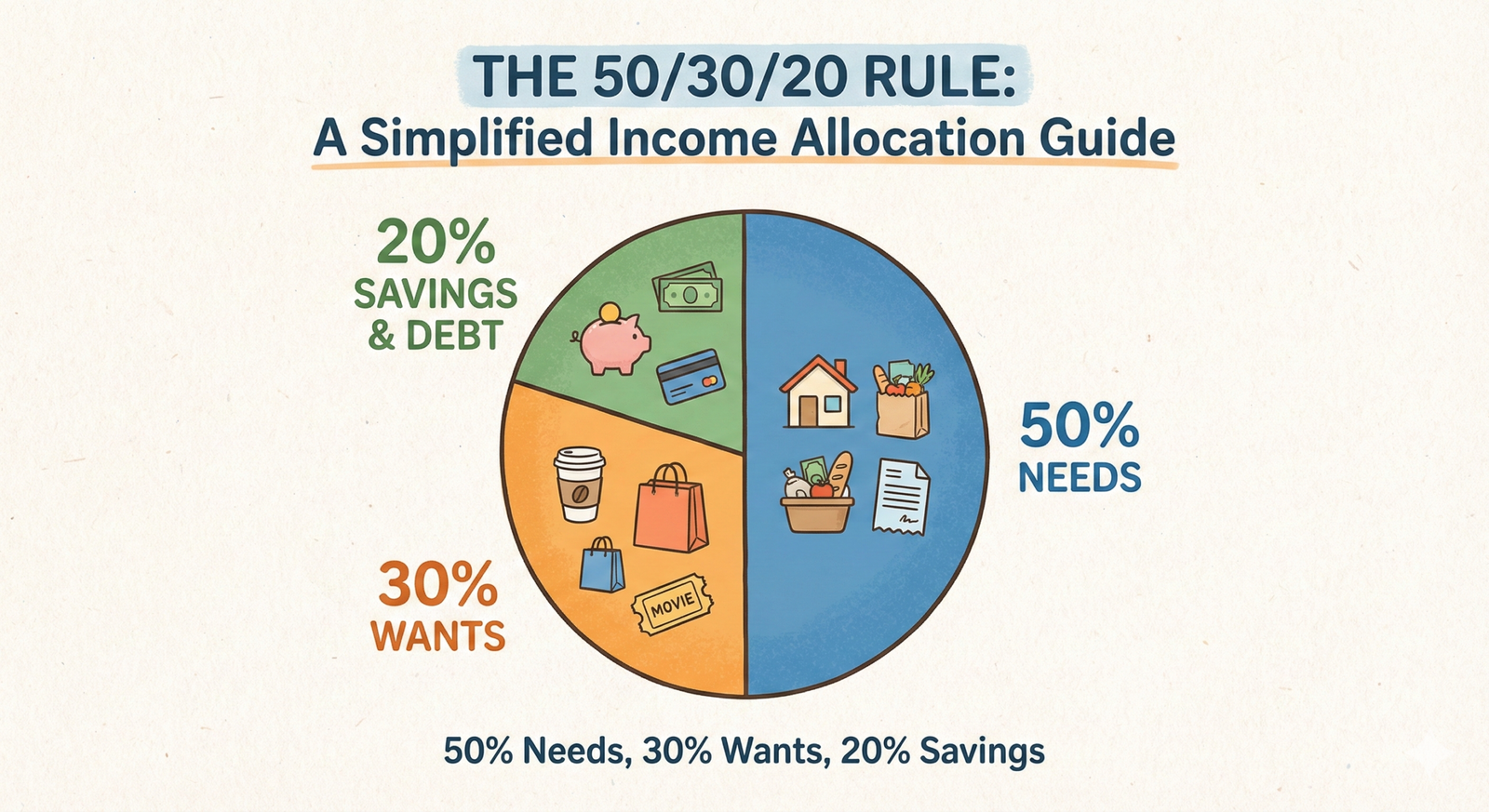

The 50/30/20 Rule

A simplified framework excellent for beginners. You prioritize 50% of your net income to Needs (The Four Walls, minimum debt payments), 30% to Wants (Discretionary spending), and 20% to Savings/Investing/Extra Debt Payoff. If your Needs exceed 50%, you must adjust your lifestyle.

10. Advanced Wealth Management: The Final Tier

Once you have mastered the foundational priorities of a budget, your cash flow will expand drastically. When you no longer have a car payment, credit card payment, or student loan payment, you will have thousands of extra dollars every month at your disposal.

At this stage, you graduate to advanced wealth management strategies. Your budget priorities shift from survival and debt reduction to asset accumulation. You may begin prioritizing real estate investing for passive cash flow, or researching the best investments 2026 to diversify your portfolio across emerging markets and technologies.

11. Conclusion: Your Budget is Your Blueprint

Understanding what should be prioritized when creating a budget transforms money from a source of stress into a tool for freedom. By establishing a rigid hierarchy—protecting your Four Walls, building an emergency shield, destroying toxic debt, paying your future self, and planning for known expenses—you mathematically guarantee your financial success.

Remember, a budget is not a static document. It is a living, breathing plan that requires monthly review. Life changes, incomes fluctuate, and emergencies happen. But as long as you adhere to this hierarchy of priorities, you will weather any economic storm and inevitably build the wealth you deserve.

Explore Advanced Wealth Building Strategies Now