ETF vs Mutual Fund: A Complete Side-by-Side Guide to Choosing the Right Investment Vehicle

Both ETFs and mutual funds let you buy a basket of investments in one transaction — but the way they’re priced, taxed, traded, and managed can make a real difference to your long-term returns. Here’s everything you need to know before you decide.

If you’ve spent any time researching how to grow your savings, you’ve almost certainly run into two terms over and over again: ETF and mutual fund. Both promise the same basic thing — instant diversification across dozens, hundreds, or even thousands of stocks and bonds, all packaged into a single investment you can buy with one click. And on the surface, that’s exactly what they deliver.

But scratch beneath that surface and you’ll find two very different financial products, each with its own rules for pricing, trading, taxation, and cost. Choosing the wrong one for your situation won’t necessarily sink your portfolio, but it can quietly cost you money over time — through higher fees, unexpected tax bills, or a structure that simply doesn’t match how you like to invest.

This guide breaks down everything you need to know about ETFs (exchange-traded funds) versus mutual funds, in plain English. We’ll walk through how each one works, where the real differences lie, and — most importantly — how to decide which one fits your personal financial goals. Whether you’re opening your first brokerage account or rebalancing a portfolio you’ve held for years, by the end of this article you’ll have a clear framework for making that decision with confidence.

Before diving in, it’s worth noting that this comparison sits inside a much bigger picture of personal finance. If you haven’t yet nailed down your broader strategy, it may help to first review some financial planning tips or explore where to put your money for the best long-term results. Understanding ETFs and mutual funds is one piece of a much larger puzzle — but it’s an important one.

1. What Are ETFs and Mutual Funds?

At their core, both an ETF (Exchange-Traded Fund) and a mutual fund are “pooled investment vehicles.” That’s a fancy way of saying that your money is combined with money from thousands of other investors, and that combined pool is used to buy a diversified collection of assets — typically stocks, bonds, or a mix of both.

Instead of having to research and purchase 50 or 500 individual stocks yourself (and then track all of them), you buy a single share of the fund, and that one share gives you proportional ownership of everything inside it. This is the foundation of modern diversified investing, and it’s why both products have become so popular with everyday investors.

ETFs in Plain English

An ETF is a basket of securities that trades on a stock exchange — just like an individual stock. You can buy or sell shares of an ETF any time the market is open, and the price moves throughout the trading day based on supply, demand, and the value of the underlying assets. Most ETFs track an index (like the S&P 500), though actively managed ETFs also exist.

Mutual Funds in Plain English

A mutual fund is also a basket of securities, but it doesn’t trade on an exchange. Instead, you buy and sell shares directly from the fund company (or through a brokerage acting on your behalf), and all transactions for the day are settled at a single price — the Net Asset Value (NAV) — calculated after the market closes. Mutual funds can be passively managed (index funds) or actively managed by a professional portfolio manager trying to beat the market.

Mutual Fund = a fund that trades like an order placed with a company, priced once per day after market close.

This single structural difference — how and when you can buy or sell — cascades into nearly every other distinction between the two products, from cost to taxation to flexibility. Understanding it is the key to understanding everything else in this guide.

For readers who are still building their foundational knowledge of investing terminology, it may also help to review the basics of the accounting equation and how the golden rules of accounting apply to how funds report their holdings and valuations.

New to Investing? Start With the Right Foundation

Build your knowledge with one of the most recommended beginner investing guides on Amazon — clear explanations, real examples, and no jargon overload.

Check Price on Amazon2. How ETFs and Mutual Funds Actually Work

To really understand the differences between these two products, it helps to understand the “behind the scenes” mechanics of each — how shares are created, how prices are set, and how your money actually moves when you place an order.

How ETF Shares Are Created and Traded

ETFs use a unique mechanism called the “creation and redemption” process. Large institutional players, known as “authorized participants,” can create new ETF shares by delivering a basket of the underlying securities to the ETF provider, or redeem shares by doing the reverse. This process happens “in kind” — meaning securities are exchanged for ETF shares rather than cash — and it’s a major reason ETFs tend to be more tax-efficient (more on that later).

For everyday investors, none of this complexity is visible. You simply log into your brokerage account, enter a ticker symbol (like VOO or QQQ), choose how many shares to buy, and place a market or limit order — exactly like buying a stock. The price you see is live, updating throughout the trading day as buyers and sellers transact.

How Mutual Fund Shares Are Created and Traded

Mutual funds work differently. When you place an order to buy or sell, that order doesn’t execute immediately at a visible market price. Instead, it’s queued up and executed at the end of the trading day, once the fund calculates its Net Asset Value (NAV). The NAV is simply:

| Component | Description |

|---|---|

| Total Assets | Sum of the market value of every security the fund holds |

| Minus Liabilities | Any fund expenses or obligations owed |

| Divided by Shares Outstanding | Total number of shares held by all investors |

| = NAV per Share | The price at which all orders for that day are filled |

This means that if you submit a buy or sell order for a mutual fund at 10am, you won’t actually know the exact price you got until after the market closes that evening. For long-term investors who aren’t trying to time short-term price movements, this rarely matters in practice — but it’s a meaningful structural difference for anyone who values intraday flexibility.

Why This Matters for You

The creation/redemption mechanism for ETFs and the once-daily pricing of mutual funds aren’t just technical trivia. They directly impact the costs you pay, how taxes are triggered, and how easily you can enter or exit a position. Keep this distinction in mind as we move through the rest of this guide — it’s the thread that connects almost every comparison point ahead.

If you’re also exploring how these vehicles fit into a broader wealth-building plan, you may find it useful to review wealth management strategies or compare options like index funds vs mutual funds, since index funds often blur the line between the two categories discussed here.

3. Key Differences at a Glance

Before we dig into each topic individually, here’s a high-level comparison table you can bookmark and refer back to. This snapshot covers the most commonly asked-about factors side by side.

| Feature | ETF | Mutual Fund |

|---|---|---|

| Trading method | Trades on an exchange like a stock | Bought/sold directly through the fund company |

| Pricing frequency | Real-time, throughout the trading day | Once daily, after market close (NAV) |

| Minimum investment | Price of one share (often less with fractional shares) | Often $500–$3,000+ minimum |

| Expense ratios | Typically lower, especially for index ETFs | Can be higher, especially actively managed funds |

| Tax efficiency | Generally more tax-efficient | Can trigger more frequent capital gains distributions |

| Management style | Mostly passive, but active ETFs exist | Both passive (index) and active options widely available |

| Automatic investing | Limited (depends on broker) | Easy to set up recurring automatic purchases |

| Trading flexibility | Can use limit orders, stop orders, intraday trades | Only one price per day, no intraday trading |

| Transparency of holdings | Usually disclosed daily | Often disclosed monthly or quarterly |

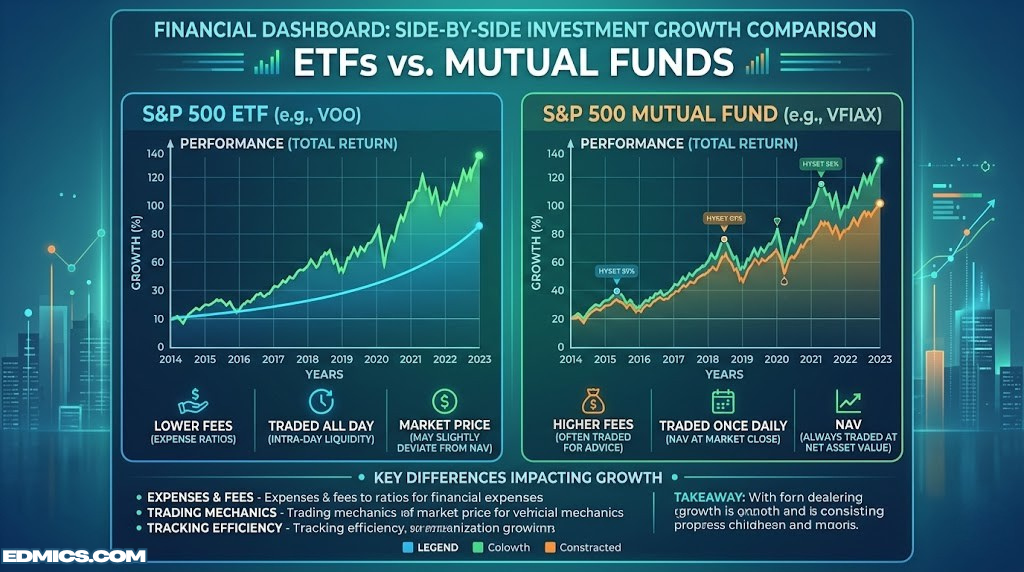

At a glance, ETFs tend to win on flexibility, cost, and tax efficiency, while mutual funds often win on simplicity for automatic, hands-off investing — particularly inside employer retirement plans. But as with most financial decisions, the “right” answer depends heavily on your specific goals, account type, and investing habits. Let’s unpack each of these rows in more detail.

It’s also worth understanding how these products fit into the bigger picture of stocks vs bonds as an investment, since both ETFs and mutual funds can hold either — or a blend of both — depending on the fund’s stated strategy.

4. Trading, Pricing & Liquidity

One of the most practical differences between ETFs and mutual funds comes down to a simple question: when can you actually buy or sell, and at what price?

Intraday Trading vs End-of-Day Settlement

Because ETFs trade on an exchange, their prices fluctuate continuously during market hours — just like Apple or Microsoft stock. If the market drops sharply at 11am and you want to sell immediately to limit losses, you can do that with an ETF. With a mutual fund, your sell order would still execute at that day’s closing NAV, regardless of what happened during the day.

This doesn’t mean intraday trading is automatically “better” — in fact, for long-term investors, the ability to react instantly to short-term price swings can sometimes encourage emotional, costly decisions. But for those who want that flexibility (or who use more advanced order types), ETFs offer it and mutual funds simply don’t.

Order Types Available

| Order Type | ETF | Mutual Fund |

|---|---|---|

| Market order | ✅ Yes | ✅ Yes (executes at end-of-day NAV) |

| Limit order | ✅ Yes | ❌ No |

| Stop-loss order | ✅ Yes | ❌ No |

| Buy on margin | ✅ Yes (with margin account) | ❌ Generally no |

| Short selling | ✅ Yes | ❌ No |

Liquidity Considerations

Liquidity refers to how easily you can buy or sell an asset without significantly affecting its price. For large, popular ETFs (think funds tracking major indexes), liquidity is generally excellent — millions of shares change hands daily, and the difference between the buy and sell price (the “bid-ask spread”) is usually tiny.

However, smaller or more niche ETFs can have wider spreads and lower trading volume, which can slightly increase the effective cost of trading. Mutual funds, by contrast, don’t have a bid-ask spread at all — everyone gets the same NAV price, regardless of fund size, because shares are created or redeemed directly with the fund company rather than traded between investors.

For readers building out a broader financial toolkit, understanding how to reconcile a bank statement against your brokerage transactions can help you keep track of exactly when trades settled and at what price — a habit that becomes especially useful once you’re holding a mix of ETFs and mutual funds.

5. Costs, Fees & Expense Ratios

Fees might seem like a minor detail, but over decades of investing, even small percentage differences can compound into tens of thousands of dollars. Understanding the fee structures of ETFs and mutual funds is one of the most financially impactful parts of this entire comparison.

Expense Ratios Explained

An expense ratio is the annual fee a fund charges, expressed as a percentage of your investment. It covers the fund’s operating costs — management salaries, administrative expenses, marketing, and more — and is automatically deducted from the fund’s returns, so you never see a separate bill.

| Fund Type | Typical Expense Ratio Range |

|---|---|

| Passive Index ETF | 0.03% – 0.20% |

| Passive Index Mutual Fund | 0.04% – 0.25% |

| Actively Managed ETF | 0.30% – 0.75% |

| Actively Managed Mutual Fund | 0.50% – 1.50%+ |

As the table shows, the lowest-cost index ETFs and lowest-cost index mutual funds are often nearly identical in price — sometimes the mutual fund version is even cheaper for large institutional share classes. The biggest cost gap tends to appear in actively managed products, where mutual funds historically carry higher fees due to research teams, portfolio managers, and higher operational overhead.

Other Potential Costs to Watch For

- Trading commissions: Most major brokers now offer commission-free ETF and mutual fund trades, but it’s worth confirming with your specific provider.

- Bid-ask spread (ETFs only): A small, often invisible cost from the difference between buy and sell prices.

- Load fees (mutual funds): Some mutual funds — particularly older or broker-sold funds — charge a “front-end load” (a percentage taken when you buy) or “back-end load” (charged when you sell). No-load funds avoid this entirely, and they’re widely available.

- Account maintenance fees: Some mutual fund companies charge small annual fees for accounts below a certain balance.

- 12b-1 fees: A marketing/distribution fee baked into some mutual funds’ expense ratios, typically 0.25% or less.

For a deeper dive into how small percentage differences affect long-term outcomes, our guide on why earning interest on interest matters explains the compounding mechanics in more detail. You can also compare specific brokerage cost structures in our Fidelity vs Charles Schwab breakdown.

Crunch the Numbers Yourself

A reliable financial calculator makes it easy to model how expense ratios, contributions, and compounding affect your portfolio over time.

Check Price on Amazon6. Tax Efficiency Compared

Taxes are one of the most underappreciated differences between ETFs and mutual funds — and for investors holding these products in taxable (non-retirement) brokerage accounts, this section may be the most financially significant one in this entire guide.

Capital Gains Distributions

When a fund sells securities at a profit, it generally must distribute those realized gains to shareholders, who then owe taxes on them — even if they didn’t personally sell anything. This is called a “capital gains distribution,” and it can happen even in a year when the fund’s overall price went down.

Mutual funds, especially actively managed ones, tend to generate more frequent and larger capital gains distributions. This happens because portfolio managers regularly buy and sell holdings to pursue their strategy, and also because when other investors redeem shares, the fund may need to sell underlying securities to raise cash — potentially triggering gains for everyone still holding the fund.

How ETFs Minimize This Problem

Remember the “in-kind” creation and redemption process we discussed earlier? This is where it really shines. When large investors redeem ETF shares, the fund can hand over actual securities instead of cash — which means it doesn’t have to “sell” anything in a way that triggers a taxable event. This structural quirk is the primary reason ETFs are widely considered more tax-efficient than mutual funds, particularly for buy-and-hold investors in taxable accounts.

| Tax Factor | ETF | Mutual Fund |

|---|---|---|

| Capital gains distribution frequency | Rare | Common, especially with active management |

| In-kind redemptions | Yes — major tax advantage | No |

| Investor controls timing of gains? | Mostly yes — gains realized when you sell | Partially — fund-level distributions are outside your control |

| Tax-loss harvesting flexibility | Generally easier due to wide range of similar ETFs | Possible but fewer near-identical substitutes |

Does This Matter in Retirement Accounts?

If you hold your ETFs or mutual funds inside a tax-advantaged account — like a 401(k), Traditional IRA, or Roth IRA — capital gains distributions don’t create an immediate tax bill, because the account itself shields you from annual taxation. In these cases, the tax-efficiency gap between ETFs and mutual funds becomes far less important, and other factors (like expense ratios and available fund choices) should drive your decision instead.

To understand how account type interacts with these tax rules, see our detailed explanation of how to think about how much you should save for retirement and how different account types are structured.

7. Minimum Investments & Accessibility

For new investors especially, the question of “how much money do I need to start?” is often just as important as the technical pros and cons. This is an area where ETFs and mutual funds diverge significantly.

ETF Entry Costs

Because ETFs trade like stocks, you typically only need enough money to buy one share — and many brokers now support “fractional share” investing, meaning you could start with as little as $1, $5, or $10, regardless of the ETF’s per-share price. This makes ETFs extremely accessible for beginners, students, or anyone wanting to start small and build up over time.

Mutual Fund Minimums

Mutual funds, on the other hand, often impose minimum initial investment requirements. These can range from $0 (increasingly common with newer or “investor share class” funds) to $500, $1,000, $3,000, or even higher for certain institutional or specialty funds. Some funds waive minimums if you set up automatic monthly contributions, which can be a helpful workaround.

| Access Factor | ETF | Mutual Fund |

|---|---|---|

| Typical minimum investment | Price of 1 share (or less with fractional shares) | $0 – $3,000+ depending on fund |

| Fractional share support | Widely available at major brokers | Less common, but some platforms support it |

| Automatic recurring investments | Available at some brokers | Very common and easy to set up |

| Available in employer 401(k) plans | Less common | Standard offering in most plans |

Why 401(k) Plans Favor Mutual Funds

If you’ve ever looked at your employer-sponsored retirement plan and noticed that all your options are mutual funds (not ETFs), you’re not alone — this is the norm. Retirement plan administrators often build their investment menus using mutual funds because of how easily they integrate with payroll deductions, automatic rebalancing, and daily NAV-based recordkeeping systems. ETF availability inside 401(k) plans is growing but still relatively limited compared to mutual funds.

This is a great example of how the “best” choice isn’t always purely about cost or tax efficiency — sometimes it’s about what’s actually available to you. If your employer match is tied to a mutual fund lineup, that’s usually still worth taking advantage of, regardless of the general preference for ETFs in taxable accounts.

For a broader view of where to allocate money across different account types and investment vehicles, check out our guide on where to invest money and our list of best investments for various goals and timelines.

8. Active vs Passive Management

While “ETF vs mutual fund” and “active vs passive” are technically two separate questions, they’re so frequently conflated that it’s worth addressing directly. The truth is: both ETFs and mutual funds come in active and passive varieties — though the proportions differ significantly.

Passive (Index) Funds

A passive fund simply aims to replicate the performance of a specific market index — like the S&P 500, the Nasdaq-100, or a total bond market index — by holding the same securities in the same proportions as that index. There’s no portfolio manager trying to “beat the market”; the goal is simply to match it as closely (and cheaply) as possible.

The vast majority of low-cost ETFs fall into this category, which is part of why ETFs have a reputation for low fees. However, passive index mutual funds exist too, and many of them have expense ratios that rival or even beat their ETF counterparts.

Active Management

An actively managed fund employs a professional manager (or team) who selects individual securities in an attempt to outperform a benchmark index. This research-intensive approach generally costs more, which is reflected in higher expense ratios. Active management has historically been more associated with mutual funds, though “active ETFs” have grown rapidly in popularity in recent years.

| Management Style | Common in ETFs? | Common in Mutual Funds? | Typical Cost Impact |

|---|---|---|---|

| Passive / Index | Very common — most popular ETF type | Common, especially “Index” labeled funds | Lowest |

| Active | Growing segment, but still smaller share | Historically dominant approach | Highest |

| Smart Beta / Factor-Based | Common | Less common | Moderate |

For a more detailed look at how index-based approaches stack up specifically, see our dedicated comparison of index funds vs mutual funds, which goes deeper into this exact distinction.

9. Performance & Tracking Differences

A common question is: “If an ETF and a mutual fund both track the same index, will they perform identically?” The honest answer is: almost, but not exactly — and the small differences that do exist are worth understanding.

Tracking Error

“Tracking error” refers to how closely a fund’s actual returns match the returns of its target index. A few factors contribute to tracking error in both ETFs and mutual funds:

- Expense ratio drag: Fees are deducted from returns, so a fund will almost always slightly underperform its benchmark by roughly the amount of its expense ratio.

- Cash drag: Mutual funds sometimes hold small cash positions to handle daily redemptions, which can slightly reduce returns during rising markets (and slightly help during falling markets).

- Sampling vs full replication: Some funds (especially for very large indexes) use a representative sample of securities rather than holding every single one, which can introduce minor deviations.

- Timing of dividend reinvestment: ETFs and mutual funds may reinvest dividends on slightly different schedules, causing small short-term differences.

Premium/Discount to NAV (ETFs Only)

Because ETF prices are determined by market trading (not solely by the underlying NAV), they can occasionally trade at a slight premium or discount to their actual NAV — though for large, liquid ETFs, this gap is typically minuscule and self-correcting due to the creation/redemption mechanism. Mutual funds, by definition, always transact exactly at NAV, so this isn’t a consideration for them.

| Performance Factor | ETF | Mutual Fund |

|---|---|---|

| Tracks index closely? | Yes, typically very close | Yes, typically very close |

| Cash drag risk | Lower (in-kind mechanism reduces need for cash buffers) | Slightly higher in some funds |

| Premium/discount to NAV | Possible but usually negligible for large funds | Not applicable — always trades at NAV |

| Dividend reinvestment | Often requires enabling DRIP with broker | Usually automatic by default |

For the overwhelming majority of long-term investors comparing a low-cost index ETF to its mutual fund equivalent (from the same provider, tracking the same index), the real-world performance difference over many years is typically minimal — often a fraction of a percentage point, driven mostly by the expense ratio gap if one exists.

To put these performance nuances in context alongside other portfolio components, our guide on top dividend-paying stocks and real estate investing basics can help you think about how ETFs and mutual funds compare to other asset classes you might be considering.

10. Pros and Cons Breakdown

By now you’ve seen the detailed mechanics — let’s consolidate everything into a clear pros and cons format for each product type.

ETF Pros and Cons

✅ ETF Pros

- Generally lower expense ratios, especially for index funds

- Trade throughout the day with real-time pricing

- Greater tax efficiency in taxable accounts

- Lower (or no) minimum investment requirements

- Wide variety of niche, sector, and thematic options

- Access to advanced order types (limit, stop-loss)

⚠️ ETF Cons

- Requires a brokerage account capable of stock trading

- Possible (small) bid-ask spreads on less liquid ETFs

- Less common in employer 401(k) plans

- Automatic recurring investments not universally supported

- Intraday trading flexibility can encourage impulsive decisions

Mutual Fund Pros and Cons

✅ Mutual Fund Pros

- Simple to set up automatic recurring contributions

- Widely available inside employer retirement plans

- No bid-ask spread — everyone gets the same NAV price

- Wide range of actively managed strategies, if desired

- Familiar structure for long-time investors

⚠️ Mutual Fund Cons

- Often higher expense ratios, especially active funds

- Minimum investment requirements can be a barrier

- Less tax-efficient — more frequent capital gains distributions

- No intraday trading — only one price per day

- Possible load fees on certain broker-sold funds

Build a Stronger Foundation

A well-reviewed personal finance book can help tie together everything from budgeting to fund selection into one cohesive strategy.

Check Price on Amazon11. Who Should Choose Which?

Rather than declaring an overall “winner,” it’s far more useful to match each product to specific investor profiles. Here are some common scenarios and which option tends to align better with each.

The New Investor with a Small Amount to Start

If you’re starting with $50, $100, or even $25, ETFs with fractional share support often make the most sense — you can begin investing immediately without worrying about minimums. Many low-cost, broadly diversified ETFs are excellent “first investment” choices.

The Set-and-Forget Automatic Investor

If your priority is setting up a recurring monthly contribution and never thinking about it again, mutual funds have historically been easier to automate through many brokerages — though this gap has been narrowing as more platforms add ETF auto-invest features. Check your specific broker’s capabilities before deciding.

The Taxable Account Investor

If you’re investing money outside of a retirement account — money you might need access to before retirement age — the tax efficiency advantages of ETFs become especially relevant. Over many years, avoiding unnecessary capital gains distributions can meaningfully improve your after-tax returns.

The 401(k) Participant

If you’re investing through an employer-sponsored plan, you likely don’t have a choice — your options are whatever your plan offers, which is usually a curated list of mutual funds. In this case, focus on selecting the lowest-cost options available within your plan’s menu, regardless of format.

The Active Strategy Believer

If you’ve researched a specific actively managed strategy — whether a particular sector focus, factor-based approach, or manager track record — and you believe in that approach, you may find more options (and more history) in the mutual fund world, though active ETFs are catching up quickly.

The DIY Trader Who Wants Flexibility

If you like to occasionally adjust your positions, use limit orders, or react to market news during the trading day, ETFs are the clear choice — mutual funds simply don’t offer this level of intraday control.

| Investor Profile | Likely Better Fit |

|---|---|

| New investor, small starting amount | ETF |

| Set-and-forget automatic investor | Either (check broker capability) |

| Taxable brokerage account holder | ETF |

| 401(k) / employer plan participant | Mutual Fund (often the only option) |

| Active strategy believer | Mutual Fund (historically more options) |

| DIY trader wanting intraday flexibility | ETF |

If you’re still working through the bigger picture of how to allocate across goals — emergency fund, retirement, taxable investing — our guide on what to prioritize when creating a budget offers a useful step-by-step framework that can help clarify where ETFs and mutual funds each fit into your overall plan.

12. ETFs and Mutual Funds in Retirement Accounts

Retirement accounts — 401(k)s, Traditional IRAs, Roth IRAs, and similar vehicles — change the calculus significantly compared to taxable brokerage accounts. Here’s how.

Tax Drag Disappears (Mostly)

Inside a tax-advantaged account, you don’t pay taxes on capital gains distributions, dividends, or interest as they occur each year. This means the tax-efficiency advantage that ETFs typically hold over mutual funds becomes largely irrelevant inside these accounts. Your decision can shift to focus purely on: expense ratios, fund availability, and strategy alignment.

IRA Flexibility

Individual Retirement Accounts (IRAs) opened through major brokerages typically offer the full range of both ETFs and mutual funds — essentially the same universe of choices you’d have in a regular taxable account, just with the tax advantages of the IRA wrapper. This makes IRAs one of the most flexible account types for choosing between ETFs and mutual funds based purely on cost and strategy.

401(k) Constraints

As mentioned earlier, most 401(k) plans are built around mutual fund lineups due to recordkeeping and administrative considerations. If your plan offers a “self-directed brokerage window,” you may have access to ETFs as well — but for most participants, the mutual fund menu is what’s available, and the best strategy is simply identifying the lowest-cost, most appropriate options from that menu.

| Account Type | ETF Availability | Mutual Fund Availability | Tax Efficiency Matters? |

|---|---|---|---|

| Taxable Brokerage | Full access | Full access | Yes — significant |

| Traditional / Roth IRA | Full access (broker-dependent) | Full access (broker-dependent) | No — tax-deferred or tax-free |

| 401(k) / Employer Plan | Limited, plan-dependent | Standard, wide selection | No — tax-deferred or tax-free |

To better understand how different account structures fit into a complete retirement strategy, see our guide on how much you should save for retirement, and explore best investment options for various time horizons.

13. Can You Use Both Together?

One of the most overlooked aspects of this whole “ETF vs mutual fund” debate is that it doesn’t have to be either/or. Many experienced investors use both products simultaneously, simply assigning each one to the role it plays best.

A Common Hybrid Approach

A frequent pattern looks something like this: use mutual funds inside the employer 401(k) (because that’s what’s available), use ETFs inside a taxable brokerage account (for tax efficiency and flexibility), and use either ETFs or mutual funds inside an IRA (whichever has the lower-cost option for your target index or strategy).

This approach isn’t about complexity for its own sake — it’s about matching each tool to the account type and goal it serves best, without forcing a one-size-fits-all rule across your entire portfolio.

Avoiding Overlap

One thing to watch for when combining ETFs and mutual funds: overlapping holdings. If you own an S&P 500 index ETF in your brokerage account and an S&P 500 index mutual fund in your 401(k), you’re effectively doubling up on the same exposure — which isn’t necessarily bad, but it’s worth being intentional about, especially when thinking about overall diversification across your full net worth.

For more on building this kind of unified view, our article on wealth management strategies covers how to think holistically across multiple account types, and our financial planning tips guide offers additional frameworks for organizing your overall approach.

14. Common Mistakes to Avoid

Whether you ultimately choose ETFs, mutual funds, or a mix of both, there are a handful of mistakes that show up again and again among investors making this decision. Avoiding these can save you money and frustration down the road.

Mistake #1: Ignoring Expense Ratios

It’s easy to focus on past performance and overlook fees — but past performance doesn’t guarantee future results, while fees are a near-certainty every single year. Always check the expense ratio before investing, and compare it to similar alternatives.

Mistake #2: Chasing Past Performance

A fund that performed well last year (or even for the past five years) isn’t guaranteed to continue that trend. This applies equally to ETFs and mutual funds, and especially to actively managed options where a strong run can sometimes be more luck than skill.

Mistake #3: Letting Taxes Drive Every Decision in Retirement Accounts

As discussed earlier, the tax-efficiency advantage of ETFs is largely irrelevant inside IRAs and 401(k)s. Don’t overthink the ETF-vs-mutual-fund choice in these accounts at the expense of more important factors like overall cost and appropriate allocation.

Mistake #4: Trading ETFs Too Frequently

The intraday flexibility of ETFs is a feature — but it can become a bug if it encourages frequent trading based on short-term market noise. Studies consistently show that investors who trade less frequently tend to achieve better long-term results than those who try to time the market.

Mistake #5: Not Checking for Overlap

As covered in the previous section, owning similar ETFs and mutual funds across different accounts without realizing it can lead to unintentional concentration in certain sectors or indexes.

Mistake #6: Assuming “Index” Always Means “Identical”

Not all S&P 500 index funds are created equal — some use full replication, others use sampling; some have slightly different rebalancing schedules. While differences are usually tiny, they’re not always zero, so it’s worth comparing the actual historical tracking performance of similar-sounding funds.

Mistake #7: Overlooking Account-Specific Fees

Some mutual funds charge small account maintenance fees for balances below a certain threshold, or have transaction fees for early redemptions (especially in funds designed to discourage short-term trading). Always read the fund’s prospectus for these details.

For additional context on avoiding costly errors, see our guide on the purposes and advantages of an audit, which — while focused on business contexts — illustrates the broader value of periodically reviewing your financial decisions with a critical eye.

15. How to Get Started

If you’ve made it this far, you should have a much clearer sense of which product — or which combination — fits your situation. Here’s a simple, practical roadmap for taking action.

Step 1: Determine Your Account Type

Are you investing through an employer 401(k), an IRA, or a regular taxable brokerage account? This single decision shapes much of what follows, since availability and tax considerations differ across each.

Step 2: Identify Your Goal and Time Horizon

Are you investing for retirement decades away, a medium-term goal like a home down payment, or simply building general wealth with no specific timeline? Your time horizon influences both your asset allocation (stocks vs bonds) and how much weight to give to factors like tax efficiency.

Step 3: Compare Specific Funds, Not Just Categories

Rather than deciding “ETF vs mutual fund” in the abstract, compare actual funds you’re considering side by side: expense ratios, minimum investments, historical tracking performance (for index funds), and — if active — the manager’s track record and strategy.

Step 4: Open or Use Your Brokerage Account

Most major brokerages support both ETFs and mutual funds within the same account, so you likely won’t need separate accounts for each. If you don’t yet have a brokerage account, research options based on fees, available fund selection, and ease of use.

Step 5: Set Up Your Investment (and Automate If Possible)

Whether you choose an ETF or mutual fund, setting up automatic recurring contributions — even small ones — can help you build the habit of consistent investing without requiring ongoing manual effort.

Step 6: Review Periodically, But Don’t Obsess

Check in on your investments periodically — perhaps quarterly or annually — to ensure your allocation still matches your goals. But avoid checking daily or reacting to short-term market movements, which can lead to the kind of impulsive decisions we discussed earlier.

For organizing your financial documents and records as your portfolio grows, our reviews of fireproof document safes and desk organizers can help keep your financial paperwork secure and accessible. And if you’re managing your investments alongside other financial tools, our comparison of QuickBooks vs Xero may be useful if you’re also tracking business finances.

Keep Your Investment Records Organized

A dedicated financial document organizer helps you keep statements, prospectuses, and tax forms in order as your portfolio grows.

Check Price on Amazon16. Frequently Asked Questions

Is an ETF the same thing as an index fund?

Not exactly. “Index fund” describes a strategy (tracking a market index), while “ETF” describes a structure (trades on an exchange). An ETF can be an index fund, but index funds can also exist as mutual funds. Many ETFs are index funds, but not all index funds are ETFs.

Which is cheaper, an ETF or a mutual fund?

It depends on the specific funds being compared. For low-cost index funds, ETFs and mutual funds from the same provider are often very close in price — sometimes the mutual fund is even slightly cheaper for certain share classes. The bigger cost gap tends to appear with actively managed funds, where mutual funds have historically charged more.

Can I lose money in an ETF or mutual fund?

Yes. Both ETFs and mutual funds invest in securities like stocks and bonds, which can decline in value. Diversification reduces — but does not eliminate — risk. The value of your investment can go down as well as up.

Do ETFs pay dividends?

Yes, if the underlying securities pay dividends, the ETF typically passes those payments along to shareholders, either as cash or through automatic reinvestment (if enabled with your broker).

Why are mutual funds priced only once a day?

Mutual funds calculate their Net Asset Value (NAV) once daily, after market close, by totaling the value of all underlying holdings and dividing by the number of outstanding shares. This ensures every investor buying or selling on a given day receives the same fair price, regardless of when during the day they placed their order.

Are ETFs riskier than mutual funds?

Not inherently. Risk depends primarily on what a fund invests in (stocks, bonds, sectors, etc.) rather than its structure as an ETF or mutual fund. A bond ETF and a bond mutual fund holding similar securities will carry similar underlying risks.

Can I convert a mutual fund into an ETF?

Some fund companies have converted existing mutual funds into ETFs, typically without triggering a taxable event for shareholders, when done at the fund level. However, you generally cannot personally “convert” your individual mutual fund shares into ETF shares on your own — this would require selling and rebuying, which could have tax implications in a taxable account.

Do I need a special brokerage account to buy ETFs?

You need a brokerage account capable of trading securities on an exchange — which is the standard type of account offered by virtually all major online brokers today. The same account can typically also hold mutual funds.

What happens to my ETF or mutual fund if the company managing it goes out of business?

The underlying securities held by the fund are typically held by a separate custodian, not the fund management company itself, which provides a layer of protection. In practice, if a fund provider faces issues, funds are often transferred to another manager or liquidated, with proceeds distributed to shareholders based on NAV.

Is it better to invest a lump sum or use dollar-cost averaging?

This depends on your individual circumstances and risk tolerance. Dollar-cost averaging (investing fixed amounts at regular intervals) can smooth out the impact of market volatility and is well-suited to both ETFs and mutual funds, especially through automatic recurring contributions.

Can beginners use both ETFs and mutual funds at the same time?

Absolutely. Many investors use mutual funds in their employer retirement plan (often the only option available) while also using ETFs in a separate brokerage account or IRA. There’s no rule requiring you to pick just one format across your entire portfolio.

How do I find a fund’s expense ratio before investing?

A fund’s expense ratio is disclosed in its prospectus and fact sheet, both of which are typically available on the fund provider’s website or through your brokerage’s research tools. Most brokerage platforms also display the expense ratio directly on the fund’s summary page before you place an order.

17. Final Verdict: ETF vs Mutual Fund

After working through pricing mechanics, costs, taxes, accessibility, and management styles, the honest conclusion is this: ETFs and mutual funds are more similar than they’re often portrayed to be — but the differences that do exist are concentrated in a few specific, high-impact areas.

If you’re investing in a taxable brokerage account and want maximum flexibility, low minimums, and strong tax efficiency, low-cost index ETFs are typically the more favorable choice. If you’re investing through an employer retirement plan, you’ll likely be working with mutual funds by default — and that’s perfectly fine, especially when paired with a focus on selecting the lowest-cost options available in your plan’s lineup.

For many investors, the real answer isn’t “ETF or mutual fund” — it’s “both, in the accounts where each makes the most sense.” A 401(k) full of low-cost mutual funds, paired with a taxable brokerage account built around tax-efficient ETFs, is a completely reasonable and common strategy.

What matters most, ultimately, isn’t the wrapper — it’s the underlying strategy, the cost, and your consistency over time. A diversified, low-cost portfolio that you contribute to regularly and hold through market ups and downs will likely serve you far better than the “perfect” choice between two similar products that you spend months agonizing over.

As you continue building your financial knowledge, you might also explore related topics like understanding balance sheets, double-entry bookkeeping, or how accounting basics tie into reading fund reports and prospectuses. The more comfortable you become with these foundational concepts, the more confident you’ll feel evaluating any investment product — ETF, mutual fund, or otherwise.

Ready to Put This Knowledge to Work?

Whether you’re opening your first investment account or fine-tuning a portfolio you’ve held for years, the most important step is the next one. Explore tools and resources that can help you compare funds, calculate fees, and stay organized along the way.

Explore Recommended Resources