Accounts Payable vs Receivable:

The Complete Financial Guide

Everything your business needs to know — from definitions and journal entries to cash flow impact, turnover ratios, and best practices for managing both sides of the ledger.

What Accounts Payable and Receivable Actually Mean for Your Business

At the center of almost every business’s financial health sit two accounts that most people confuse, conflate, or simply mismanage: accounts payable and accounts receivable. These two ledger items represent opposite sides of the same credit-based transaction — and understanding how they work, interact, and differ is one of the most important foundations in all of accounting.

Whether you run a small retail store, manage the books for a mid-size manufacturer, or are studying for a finance exam, you cannot escape the AP vs AR question. Together, they determine how fast money moves through your business, how much working capital you have at any moment, and whether your cash flow statement tells a healthy story or a concerning one.

This guide cuts through the jargon. By the time you finish reading, you will be able to record both types of transactions correctly, analyze their impact on financial statements, build efficient collection and payment processes, and use key ratios to benchmark your performance. If you are just beginning your accounting journey, our Accounting Basics 101 primer provides excellent grounding before diving deeper here.

The relationship between AP and AR is deeply intertwined with concepts like the accounting equation, the double-entry bookkeeping system, and the way a business’s balance sheet is structured. Understanding it fully means understanding how money really flows through an organization — not just when cash changes hands, but when obligations are created and when rights to collect are earned.

QuickBooks Online — Automate Your AP & AR

Streamline invoicing, track outstanding balances, and manage vendor payments from one dashboard. Trusted by over 7 million businesses.

🛒 Check Price on AmazonAccounts Payable and Accounts Receivable: Core Definitions

Before analyzing the differences, you need rock-solid definitions of each term. These are not interchangeable concepts with slight nuances — they describe fundamentally opposite financial positions.

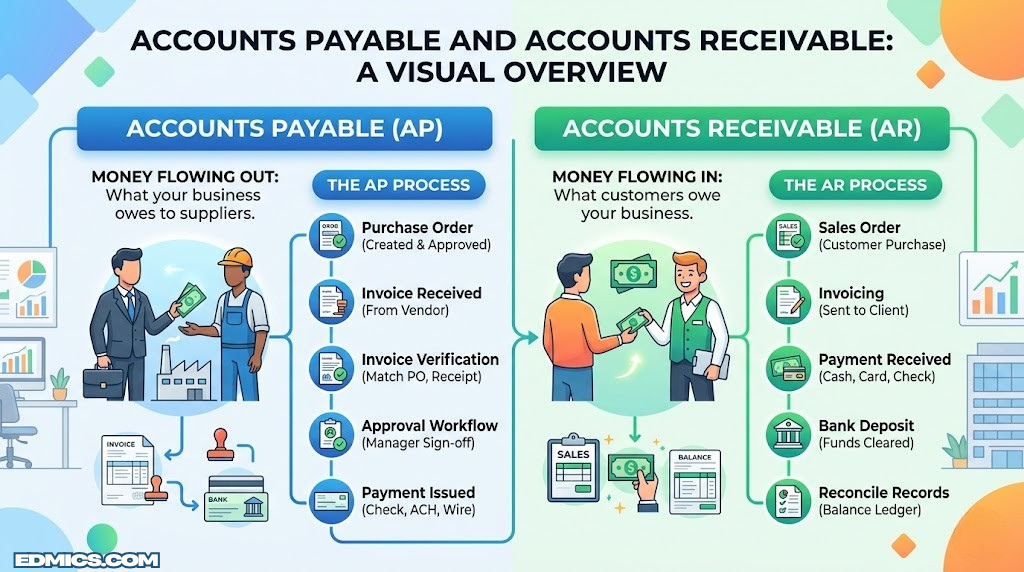

Accounts Payable (AP)

Money your business owes to suppliers, vendors, or creditors for goods or services you have already received but not yet paid for. It is a current liability on your balance sheet.

Example: You order $5,000 in raw materials from a supplier on Net 30 terms. Until you pay that invoice, $5,000 sits in accounts payable.

Balance Sheet: LIABILITY ↓Accounts Receivable (AR)

Money owed to your business by customers for goods or services you have already delivered but not yet collected payment for. It is a current asset on your balance sheet.

Example: You deliver $8,000 in consulting services to a client on Net 30 terms. Until they pay, $8,000 sits in accounts receivable.

Balance Sheet: ASSET ↑The Credit-Based Business Cycle

Both AP and AR exist because of trade credit — the common business practice of delivering goods or services before payment is received. Without trade credit, every transaction would require immediate cash exchange, which would dramatically slow commerce and limit business growth.

When Company A sells to Company B on credit, Company A records an accounts receivable (an asset — it is owed money) and Company B records an accounts payable (a liability — it owes money). Same invoice, same dollar amount, two completely different accounting entries on two different sets of books. This mirrors the logic of the golden rules of accounting — every debit has a corresponding credit, and every liability for one party is an asset for another.

What Qualifies as Accounts Payable?

Not every obligation a business has falls under accounts payable. AP specifically refers to short-term trade payables — amounts owed to suppliers and vendors for regular business operations. Common examples include:

- Invoices from raw material suppliers

- Utility bills (electricity, water, internet) received but unpaid

- Rent obligations for the current period not yet paid

- Professional service fees (legal, accounting, IT) on invoice

- Office supplies and consumables ordered on credit

Long-term debts (bank loans, bonds payable) are not accounts payable — they are classified separately as long-term liabilities.

What Qualifies as Accounts Receivable?

Similarly, not every amount coming in to a business counts as AR. Accounts receivable specifically represents trade receivables — amounts owed by customers for goods or services already delivered. Common examples include:

- Customer invoices for products shipped but not yet paid

- Client fees for completed services awaiting payment

- Subscription or recurring service invoices for the current period

- Sales made on store credit or installment arrangements

Cash sales, advance payments received, and prepaid subscriptions are not accounts receivable — they either involve immediate cash or create a liability (deferred revenue) rather than an asset.

Accounts Payable vs Receivable: The Key Differences at a Glance

Even seasoned professionals sometimes blur these concepts under pressure. The table below provides a comprehensive side-by-side comparison that covers every important dimension — from accounting classification to operational impact.

| Dimension | Accounts Payable (AP) | Accounts Receivable (AR) |

|---|---|---|

| Basic Definition | Money your business owes to vendors/suppliers | Money owed to your business by customers |

| Financial Classification | Current Liability | Current Asset |

| Balance Sheet Position | Right side (Liabilities & Equity) | Left side (Assets) |

| Normal Balance | Credit | Debit |

| Transaction Trigger | You receive goods/services on credit | You deliver goods/services on credit |

| Cash Flow Effect | Increase = cash conservation (positive short-term) | Increase = cash not yet received (negative short-term) |

| Key Business Function | Vendor/supplier payment management | Customer invoice & collection management |

| Risk Type | Late payment penalties, supplier relationship damage | Bad debts, slow collection, default risk |

| Key Ratio | AP Turnover / Days Payable Outstanding (DPO) | AR Turnover / Days Sales Outstanding (DSO) |

| Related Statement | Balance Sheet + Cash Flow (operating) | Balance Sheet + Cash Flow (operating) |

| Who Manages It | AP department / Finance team | AR department / Sales/Finance team |

| Allowance Account | Not typically needed | Allowance for Doubtful Accounts (contra-asset) |

The Directional Rule: Money In vs. Money Out

The easiest way to keep the two apart is to think in terms of direction of money flow. Accounts payable represents money that will eventually leave your business. Accounts receivable represents money that will eventually arrive at your business. Payable = outgoing obligation. Receivable = incoming right.

This directional thinking also clarifies their opposite effects on liquidity. When AP rises, you have more short-term obligations — but you have also preserved cash by deferring payment. When AR rises, you have more assets on paper — but you have not actually collected the cash yet, which means your liquidity may be tighter than your income statement suggests. Understanding this dynamic is essential for sound financial planning.

A Tale of Two Invoices

Consider a printing company that buys paper stock from a supplier and sells printed brochures to a marketing agency. The same day they receive $3,000 worth of paper on Net 30 terms, they send the marketing agency a $7,000 invoice for completed brochures. That single day, the printer creates:

- $3,000 in accounts payable — a liability owed to the paper supplier

- $7,000 in accounts receivable — an asset owed by the marketing agency

Their net position is $4,000 in their favor — but none of that cash has actually moved yet. This is the essence of accrual-based accounting, and it is why understanding AR and AP is inseparable from understanding how to read a balance sheet.

How AP and AR Appear on Financial Statements

One of the most important things to understand about accounts payable and accounts receivable is exactly where — and how — they appear across the three core financial statements. Each one tells a different part of the story.

The Balance Sheet

This is the primary home for both AP and AR. The balance sheet is a snapshot of a company’s financial position at a single point in time, organized according to the fundamental accounting equation: Assets = Liabilities + Equity.

| Balance Sheet Section | Line Item | Account Type | Where It Appears |

|---|---|---|---|

| Current Assets | Accounts Receivable | Asset (Debit balance) | Left side of balance sheet, below Cash |

| Current Assets (contra) | Allowance for Doubtful Accounts | Contra-Asset (Credit balance) | Directly below AR, shown in parentheses |

| Current Liabilities | Accounts Payable | Liability (Credit balance) | Right side of balance sheet, near top of liabilities |

A sample balance sheet snippet for a mid-size business might look like this:

| CURRENT ASSETS | CURRENT LIABILITIES | ||

|---|---|---|---|

| Cash & Equivalents | $42,000 | Accounts Payable | $28,500 |

| Accounts Receivable | $65,000 | Accrued Expenses | $9,200 |

| Allowance (Doubtful) | ($3,200) | Short-term Notes | $15,000 |

| Inventory | $31,000 | ||

| Total Current Assets | $134,800 | Total Current Liabilities | $52,700 |

The Income Statement

The income statement does not directly show AP or AR balances, but it is deeply connected to them. Revenue is recognized when goods or services are delivered — which is the exact moment AR is created. If AR is never collected, it becomes a bad debt expense that flows through the income statement, reducing net income. For a full walkthrough of how revenue, expenses, and income connect, our income statement guide provides clear step-by-step coverage.

The Cash Flow Statement

This is where AP and AR’s real-world cash impact becomes visible. Both appear in the Operating Activities section as adjustments to net income. The logic follows the indirect method: since net income was computed on an accrual basis, changes in working capital accounts (including AR and AP) are used to reconcile it to actual cash flow.

| Change in Working Capital | Effect on Operating Cash Flow | Why |

|---|---|---|

| Increase in AR | Decreases Cash Flow (−) | Revenue earned but cash not yet received |

| Decrease in AR | Increases Cash Flow (+) | Prior receivables have been collected |

| Increase in AP | Increases Cash Flow (+) | Expense incurred but cash not yet paid out |

| Decrease in AP | Decreases Cash Flow (−) | Prior obligations have been paid in cash |

This counterintuitive behavior — where rising AR actually hurts cash flow — is one of the most important concepts in the entire cash flow statement. A company can report record profits on its income statement while simultaneously running out of cash because customers are slow to pay. This is known as a working capital trap, and it catches even well-run businesses off guard.

Professional Financial Calculator — HP 12C

The gold standard for financial professionals. Calculate turnover ratios, NPV, IRR, and amortization schedules in seconds.

🛒 View on AmazonJournal Entries: Recording AP and AR Correctly

The double-entry bookkeeping system requires that every financial transaction affects at least two accounts — and that the total of debits always equals the total of credits. Recording accounts payable and accounts receivable correctly is foundational to any accurate set of books. Our comprehensive guide to double-entry bookkeeping walks through this system in full detail if you need a deeper foundation.

Accounts Payable Journal Entries

Accounts payable goes through two stages: creation (when the obligation is incurred) and settlement (when cash is paid).

Step 1 — Recording the Payable (When Invoice Is Received)

Suppose your business receives a $4,500 invoice from an office supplies vendor:

| Account | Debit | Credit |

|---|---|---|

| Office Supplies Expense | $4,500 | |

| Accounts Payable | $4,500 |

The expense account increases (debit), and the liability increases (credit).

Step 2 — Settling the Payable (When Cash Is Paid)

| Account | Debit | Credit |

|---|---|---|

| Accounts Payable | $4,500 | |

| Cash / Bank | $4,500 |

The liability decreases (debit), and cash decreases (credit). The obligation is cleared.

Accounts Receivable Journal Entries

Similarly, AR moves through two stages: recognition (when revenue is earned) and collection (when cash arrives).

Step 1 — Recording the Receivable (When Invoice Is Sent)

Your business sends a client a $7,200 invoice for completed graphic design services:

| Account | Debit | Credit |

|---|---|---|

| Accounts Receivable | $7,200 | |

| Revenue (Service Revenue) | $7,200 |

The asset increases (debit), and revenue increases (credit). Profit is recognized even before cash is received.

Step 2 — Collecting the Receivable (When Cash Is Received)

| Account | Debit | Credit |

|---|---|---|

| Cash / Bank | $7,200 | |

| Accounts Receivable | $7,200 |

Cash increases (debit), and the AR asset decreases (credit). The obligation is fulfilled.

Recording Bad Debts (Allowance Method)

When a customer is unlikely to pay, businesses using the allowance method record an estimated bad debt expense before the account is actually written off. This is required under GAAP’s matching principle. For a thorough look at GAAP requirements, our GAAP explained guide covers all the key standards.

| Account | Debit | Credit | Note |

|---|---|---|---|

| Bad Debt Expense | $1,800 | Income statement impact | |

| Allowance for Doubtful Accounts | $1,800 | Contra-asset on balance sheet |

This entry reduces the net realizable value of AR on the balance sheet without actually eliminating the underlying receivable — because there is still a chance the customer may pay. If the debt is eventually confirmed uncollectable, a write-off entry removes both the AR and the allowance account simultaneously.

How AP and AR Shape Your Cash Flow

Understanding the mechanics of how accounts payable and receivable affect cash flow is perhaps the single most valuable skill for any business owner or financial manager. Many businesses fail not because they are unprofitable, but because their cash flow management is poor — and both AP and AR are central characters in that story.

The Working Capital Connection

Working capital is calculated as Current Assets minus Current Liabilities. Both AR and AP directly affect this number:

A business with high AR and low AP appears to have strong working capital — but if AR is not collected promptly, that working capital is illiquid. Conversely, a business that strategically stretches AP (within terms) while aggressively collecting AR is optimizing its cash conversion cycle. This is a core concept in understanding the difference between gross and net working capital.

The Cash Conversion Cycle (CCC)

The cash conversion cycle measures how long it takes for a business to convert its investments in inventory and other resources into cash flows from sales. AP and AR are two of the three inputs:

| CCC Component | Tied To | Business Goal |

|---|---|---|

| Days Sales Outstanding (DSO) | Accounts Receivable | Minimize (collect faster) |

| Days Inventory Outstanding (DIO) | Inventory | Minimize (sell faster) |

| Days Payable Outstanding (DPO) | Accounts Payable | Maximize (pay slower — within terms) |

Strategic Tension: When AP and AR Pull in Opposite Directions

The best-run businesses actively manage the gap between when they collect from customers (AR) and when they pay their suppliers (AP). If customers pay in 60 days but suppliers expect payment in 30 days, the business has a 30-day funding gap — it must bridge that gap with its own cash reserves or a line of credit.

This is why large corporations often negotiate longer payment terms with smaller suppliers while enforcing strict collection timelines with their own customers. It is a form of free short-term financing — sometimes called trade credit optimization. Thoughtful management here is a pillar of any serious wealth management strategy at the enterprise level.

Professional Accounting Ledger Book — Adams Money & Rent Record

Track payables, receivables, and all business income and expenses in an organized, professional format. A must-have for small business bookkeepers.

🛒 See on AmazonTurnover Ratios: Measuring AP and AR Efficiency

Ratios are the language of financial performance benchmarking. For both accounts payable and accounts receivable, there are two primary ratios — one that measures speed in absolute terms (the turnover ratio) and one that translates that speed into days (DPO or DSO). These ratios are critical for anyone serious about strategic financial planning.

Accounts Receivable Turnover Ratio

This ratio tells you how many times during a period your business fully collects its average outstanding AR balance. A higher number is better — it means customers are paying quickly and you are cycling through your receivables efficiently.

Days Sales Outstanding (DSO)

Example: If a business has net credit sales of $480,000 and average AR of $80,000, the AR turnover is 6 times, giving a DSO of about 61 days. This means the business takes roughly two months to collect each invoice — which may or may not be acceptable depending on its industry and payment terms.

Accounts Payable Turnover Ratio

This ratio measures how quickly a business pays its suppliers. Unlike AR turnover (where higher is better), AP turnover interpretation depends on strategy. Too high may mean you are paying suppliers faster than necessary, hurting liquidity. Too low may signal cash flow problems or strained supplier relationships.

Days Payable Outstanding (DPO)

Benchmark Comparison Table

| Metric | Formula | Healthy Range | Warning Signal |

|---|---|---|---|

| AR Turnover | Net Credit Sales / Avg AR | 6–12× per year | Below 4× (slow collection) |

| DSO | 365 / AR Turnover | 30–45 days | Over 60 days (risk of bad debt) |

| AP Turnover | Total Purchases / Avg AP | 6–10× per year | Below 4× (cash flow issues) |

| DPO | 365 / AP Turnover | 30–60 days | Over 90 days (supplier friction) |

The ideal scenario is a business with a DSO shorter than its DPO — meaning it collects from customers before it must pay suppliers. This creates a naturally positive cash conversion cycle and minimizes reliance on external financing. These ratios also matter deeply to investors and lenders evaluating business health, which is why tracking them is a core component of our balance sheet reading guide.

Managing Accounts Payable: Best Practices and Strategies

Effective accounts payable management is not simply about paying bills on time. Done strategically, it becomes a tool for preserving liquidity, building supplier relationships, capturing early payment discounts, and avoiding late fees. Here is how high-performing finance teams handle AP.

Core AP Management Best Practices

- 1Centralize Invoice Processing

All vendor invoices should flow through one system or team to prevent duplicates, missed payments, and unauthorized obligations. Accounting software like QuickBooks or Xero automates invoice capture and matching.

- 2Implement Three-Way Matching

Before approving any payment, match the purchase order, receiving report, and vendor invoice. This prevents overpayments, fraud, and billing errors — a critical internal control for any business following solid management principles.

- 3Capture Early Payment Discounts

Many suppliers offer a 2/10 Net 30 arrangement — a 2% discount for payment within 10 days. On a $50,000 invoice, that is $1,000 saved. Annualized, this 2% discount over 20 days represents an effective annual return of approximately 36%.

- 4Negotiate Favorable Payment Terms

Rather than accepting standard 30-day terms, negotiate Net 45 or Net 60 with suppliers where possible. Extended terms improve your DPO without damaging the relationship, giving you more time to collect from your own customers first.

- 5Set Up Payment Approval Workflows

Require dual approval for payments above a threshold. This prevents fraud, unauthorized expenditures, and errors while keeping the AP process moving efficiently.

- 6Run Aging Reports Weekly

An AP aging report shows all outstanding invoices grouped by how long they have been outstanding (current, 1–30 days, 31–60 days, 61–90 days, 90+ days). Reviewing this weekly ensures nothing slips through the cracks or becomes overdue.

Pros and Cons of Extended AP Terms

✅ Pros of Stretching AP

- Preserves cash for operations and growth

- Reduces need for short-term borrowing

- Improves DPO and cash conversion cycle

- Free supplier financing within agreed terms

- Better liquidity ratios for investors

❌ Cons of Stretching AP

- Damages supplier relationships if overdone

- Risks supply chain disruption if suppliers cut credit

- Forfeits early payment discounts

- Late fees reduce margins if terms are breached

- Signals financial distress to credit analysts

Managing Accounts Receivable: Best Practices and Strategies

Accounts receivable management is fundamentally about converting credit sales into cash as quickly as possible — without damaging customer relationships. A slow AR process is one of the most common causes of cash flow strain in otherwise healthy businesses.

AR Management Best Practices

- 1Establish a Clear Credit Policy

Before extending credit to any customer, define your criteria: credit limits, payment terms, required documentation, and acceptable risk levels. Tightening credit standards upfront is far less costly than chasing bad debts later. This aligns with the broader budgeting discipline of planning for worst-case scenarios.

- 2Invoice Immediately and Accurately

Every day you delay sending an invoice is a day added to your DSO. Modern AR software can generate and deliver invoices the same day services are rendered. Accuracy matters too — errors on invoices give customers legitimate reasons to delay payment while disputes are resolved.

- 3Offer Multiple Payment Options

Accept ACH transfers, credit cards, online payments, and bank transfers. Friction in the payment process adds days to your DSO. The easier you make it to pay, the faster customers will do it.

- 4Send Automated Payment Reminders

Set up automated email reminders at 7 days before due, on the due date, and at 7, 14, and 30 days past due. Automation removes the awkwardness of chasing customers manually and keeps collections consistent regardless of staff capacity.

- 5Offer Early Payment Incentives

Just as suppliers offer you 2/10 Net 30, you can offer your customers the same deal. A 1–2% discount for early payment is often worth it to accelerate your cash inflows and reduce bad debt exposure.

- 6Run AR Aging Reports Weekly

Your AR aging report shows outstanding invoices grouped by age — current, 1–30, 31–60, 61–90, and 90+ days. Invoices in the 60+ bucket require immediate escalation because the probability of collection drops sharply after 90 days.

When to Consider AR Factoring

If your AR balance is large and your customers are consistently slow payers, accounts receivable factoring (or invoice financing) allows you to sell your invoices to a factoring company at a discount in exchange for immediate cash. This strategy sacrifices some margin but provides immediate liquidity. It is particularly common in industries like staffing, manufacturing, and construction where payment cycles are long. Think of it as a form of alternative capital management — turning a future asset into present cash at a cost.

Epson EcoTank All-in-One Printer — Invoice & Report Printing

Print professional invoices, AR aging reports, and financial documents in-house. High-capacity ink tanks reduce cost per page dramatically. See our full review here.

🛒 Check Price on AmazonCommon Mistakes Businesses Make with AP and AR

Even finance teams with years of experience make consistent, predictable mistakes in managing payables and receivables. Knowing the most common pitfalls is the first step to avoiding them.

Accounts Payable Mistakes

| Mistake | Consequence | Fix |

|---|---|---|

| Paying the same invoice twice | Cash leak, reconciliation headache | Three-way matching + duplicate invoice detection |

| Missing early payment discount windows | Lost savings (can be 20–36% annualized) | Prioritize discount-eligible invoices in payment queue |

| No vendor master file reconciliation | Ghost vendors, fraud risk | Quarterly vendor master audit with management sign-off |

| Paying before goods are verified received | Pay for goods that never arrive | Enforce three-way match before approving payment |

| Manual AP processes at scale | Errors, slow processing, staff overload | Automate with accounting software or AP automation tools |

Accounts Receivable Mistakes

| Mistake | Consequence | Fix |

|---|---|---|

| Extending credit without checking customer history | High bad debt expense, cash flow damage | Formal credit assessment for every new customer |

| Delayed invoicing after service delivery | Artificially inflated DSO | Invoice same-day or within 24 hours of delivery |

| No escalation process for overdue accounts | Invoices age into uncollectable territory | Documented collections procedure with trigger dates |

| Writing off bad debts late or inaccurately | Overstated AR, misleading financial statements | Regular review with allowance for doubtful accounts |

| Accepting only one payment method | Payment friction adds days to DSO | Accept ACH, card, wire, and online payment portals |

The Biggest Cross-Functional Mistake

Perhaps the most costly error is treating AP and AR as isolated departmental functions with no visibility into each other. In reality, they are deeply interconnected through working capital, the cash conversion cycle, and the company’s overall liquidity position. Finance teams that reconcile and analyze both together — in the same weekly or monthly management meeting — make dramatically better decisions about when to accelerate payments, when to push collections, and when to draw on credit lines. This integrated view is central to strong financial management practice.

Software Tools for Managing AP and AR

The right software transforms AP and AR management from a manual, error-prone chore into an automated, real-time system that improves with scale. The market offers tools for every business size and budget.

Comparison of Leading AP/AR Software Solutions

| Software | Best For | AP Features | AR Features | Pricing Tier |

|---|---|---|---|---|

| QuickBooks Online | Small–mid businesses | Invoice processing, bill pay, aging reports | Invoicing, reminders, payment portals | Mid-range |

| Xero | Small businesses, global users | Bill tracking, payment scheduling | Branded invoices, Stripe integration | Mid-range |

| FreshBooks | Freelancers, service businesses | Basic bill management | Recurring invoices, automatic reminders | Budget-friendly |

| SAP S/4HANA | Enterprise corporations | Full AP automation, vendor portal | Advanced AR analytics, dunning management | Enterprise |

| Bill.com | SMBs focused on AP automation | Two-way sync, approval workflows | Basic AR collection tools | Mid-range |

| Zoho Books | Small businesses, startups | Vendor bills, payment tracking | Client invoices, online payments | Budget-friendly |

For a direct head-to-head between the two most popular choices for small businesses, our QuickBooks vs FreshBooks comparison and QuickBooks vs Xero breakdown cover every key dimension in detail. Tax preparation software is a separate but related consideration — see our TurboTax vs H&R Block guide for tax filing choices once your AP and AR records are in order.

What to Look for in AP/AR Software

Keeping your documents and financial records secure is another consideration. Our review of the top fireproof document safes covers physical storage options for sensitive financial records that should always have a backup off your digital system.

Real-World Examples: AP and AR in Action Across Industries

Abstract definitions come alive when placed in real industry contexts. The following examples show how accounts payable and accounts receivable function differently — and with different urgency — depending on the business model.

Manufacturing Company

A furniture manufacturer buys $120,000 in raw wood and hardware from three suppliers each month (creating AP), while selling $310,000 in finished furniture to retail chains on 45-day credit terms (creating AR). The business must manage a 45-day collection cycle and 30-day payment cycle — a 15-day positive gap. If a retail chain delays payment, the manufacturer may need a line of credit to cover supplier payments without disrupting the supply chain. This is a textbook case of why cash flow management matters even in a profitable business.

Professional Services Firm (Law / Accounting)

A mid-size law firm bills clients monthly on net 30 terms. Partners spend heavily on office rent, legal research subscriptions, and staff salaries (creating various payables), while the firm’s AR may stretch to 60–90 days because legal billing is frequently disputed or delayed. Firms in this position often maintain a significant credit facility specifically to bridge the AR collection gap. Our guide to best desk organizers and leather padfolios covers tools that keep busy professionals like these organized amid heavy paperwork loads.

Retail Business

A small retail boutique operates primarily with cash and card sales — meaning very little AR (most sales are immediate cash transactions). However, its AP can be substantial, as it orders inventory from suppliers on credit. The retailer’s priority is managing AP well — capturing discounts, maintaining supplier relationships, and avoiding stockouts due to credit issues.

E-Commerce / Online Seller

An Amazon third-party seller using FBA has minimal direct AR (Amazon disburses sales proceeds on a two-week schedule, making this more like a receivable from a single, reliable counterparty). AP includes inventory purchases, advertising fees, fulfillment costs, and software subscriptions. For sellers growing this type of business, understanding how AP and AR relate to working capital is essential reading alongside our real estate investing guide for diversifying beyond e-commerce.

Construction Industry

Construction companies face some of the most complex AP/AR situations of any industry. Projects may span months or years; billing happens in stages tied to project milestones (progress billing); subcontractors must be paid (AP) on different timelines than when the general contractor collects from property owners (AR). Retainage clauses further complicate AR by withholding 5–10% of each progress payment until project completion. Tight AP/AR management is literally the difference between project profitability and bankruptcy in construction.

These real-world contexts reinforce a core truth: accounts payable and accounts receivable are not just accounting line items. They are the financial expression of how a business interacts with every supplier and customer it works with. Managing them well requires understanding both the accounting mechanics and the business relationships behind each invoice. For those looking to sharpen their broader financial analysis skills, our guides on bank statement reconciliation and depreciation in accounting provide essential next steps.

Frequently Asked Questions: Accounts Payable vs Receivable

Q1What is the main difference between accounts payable and accounts receivable?

Accounts payable represents money your business owes to suppliers or vendors for goods and services received on credit — it is a current liability. Accounts receivable represents money owed to your business by customers for goods or services already delivered — it is a current asset. The simplest way to remember it: payable = you pay, receivable = you receive.

Q2Where do AP and AR appear on financial statements?

Accounts payable appears as a current liability on the balance sheet. Accounts receivable appears as a current asset on the balance sheet. Both affect the operating activities section of the cash flow statement as working capital adjustments. They do not appear directly on the income statement, though bad debt expense from uncollectable AR does flow through it.

Q3Can AP and AR be the same amount?

Mathematically, yes — though practically rare within a single company. When two companies trade with each other, one company’s AP is exactly mirrored by the other company’s AR on the same invoice. Within a single business, the AP and AR balances reflect entirely different sets of transactions and will rarely be identical.

Q4What is a normal payment term for accounts payable?

The most common AP payment term is Net 30, meaning payment is due within 30 calendar days of the invoice date. Other common terms include Net 15, Net 45, Net 60, and Net 90. Early payment discount terms like 2/10 Net 30 (2% discount if paid within 10 days, otherwise full amount due in 30) are also widely used. The specific terms depend on the industry and the negotiated agreement between buyer and supplier.

Q5How does accounts receivable affect cash flow?

An increase in AR reduces operating cash flow because revenue has been earned but cash has not yet been received. A decrease in AR boosts cash flow as customers pay their outstanding invoices. On the cash flow statement (indirect method), changes in AR are shown as adjustments to reconcile net income to actual cash generated from operations.

Q6What is the AR turnover ratio and how is it calculated?

The AR turnover ratio measures how efficiently a business collects its receivables during a period. It is calculated as Net Credit Sales divided by Average Accounts Receivable (beginning AR plus ending AR, divided by 2). A higher ratio indicates faster collection. Dividing 365 by the AR turnover ratio gives you Days Sales Outstanding — the average number of days to collect each invoice.

Q7What is a bad debt, and how is it recorded?

A bad debt occurs when a customer is unable or unwilling to pay their outstanding invoice. Under the allowance method (required by GAAP), businesses estimate bad debts in advance and record them as Bad Debt Expense with a corresponding credit to Allowance for Doubtful Accounts — a contra-asset that reduces the net AR balance on the balance sheet. When a specific account is confirmed uncollectable, the AR balance and the allowance are both reduced (written off) simultaneously.

Q8Should small businesses have separate AP and AR departments?

Most small businesses handle both functions within a single accounting role or a small team. As the business grows in transaction volume and complexity, separating AP and AR into dedicated roles improves internal controls, reduces the risk of fraud (one person should not control both payment and collection), and allows each function to be optimized independently. A clear segregation of duties is one of the most important internal control best practices regardless of business size.

Q9What is the AP turnover ratio?

The AP turnover ratio measures how many times a business pays off its average AP balance in a given period. It is calculated as Total Supplier Purchases divided by Average Accounts Payable. A high AP turnover indicates prompt payment; a lower ratio may signal cash constraints or intentional payment extension within terms. Days Payable Outstanding (DPO) is calculated as 365 divided by AP turnover and represents the average number of days a business takes to pay each supplier invoice.

Q10What software tools are best for managing AP and AR?

Popular choices include QuickBooks Online, Xero, FreshBooks, Bill.com, and Zoho Books for small to mid-size businesses, and SAP S/4HANA or Oracle Financials for enterprise-level operations. The best choice depends on your transaction volume, integration needs, budget, and whether you prioritize AP automation (Bill.com) or balanced AP/AR functionality (QuickBooks, Xero).

Q11What is the difference between AR and notes receivable?

Accounts receivable are informal, short-term trade obligations — typically settled within 90 days — with no formal written promise beyond the invoice itself. Notes receivable are formal, written promissory notes in which the debtor commits in writing to pay a specific amount by a specific date, often with interest. Notes receivable may extend beyond one year and are classified as long-term assets when they do, unlike AR which is always current.

Q12How do AP and AR relate to the accounting equation?

Accounts payable increases the liabilities side of the accounting equation (Assets = Liabilities + Equity), while accounts receivable increases the assets side. They represent opposite aspects of credit-based transactions within the double-entry bookkeeping system. Every AP entry has a corresponding debit to an expense or asset account, and every AR entry has a corresponding credit to a revenue account — keeping the equation in perfect balance at all times.

Master Both Sides of Your Ledger — Start Today

Accounts payable and accounts receivable are not just accounting line items — they are the financial pulse of your business. Managing them with precision means better cash flow, stronger supplier relationships, faster customer collection, and a balance sheet that tells a clear, confident story to investors and lenders alike.

Whether you are a small business owner just learning the ropes, a finance student building your foundation, or an experienced bookkeeper looking to sharpen your practice, the concepts in this guide are the building blocks everything else rests on.

📚 Explore Accounting Basics 101 →Continue Learning: Related Finance Guides

Your AP and AR knowledge connects to a broader ecosystem of financial literacy. Here are the most directly related resources to deepen your understanding:

- Double-Entry Bookkeeping: The Complete Guide — The foundational system behind every AP and AR journal entry

- Understanding Balance Sheets: A Beginner’s Guide — Where AP and AR live and how they interact with other accounts

- Income Statement Guide — How AR drives revenue recognition and bad debts hit your bottom line

- Cash Flow Statement Guide — Where AP and AR changes appear and how to interpret them

- GAAP Explained — The accounting standards that govern how AP and AR must be recorded

- QuickBooks vs Xero — Choosing the right software to automate your AP/AR workflows

- How to Reconcile a Bank Statement — The monthly process that ties your AP/AR records to actual cash

- Financial Planning Tips — Building AP/AR strategy into your broader business financial plan

- Purposes and Advantages of Audit — Why auditing your AP and AR processes protects the business

- Best Calculators for Finance — Tools for computing turnover ratios, DSO, DPO, and cash flow metrics