Investing Basics · Asset Classes Compared

Stocks vs Bonds: How to Split Your Money Between Growth and Stability

Two of the oldest tools in investing, explained side by side — how each one actually makes you money, what can go wrong, and how much of each belongs in your own portfolio.

Two assets, one decision: how much growth versus how much stability does your money need right now?

Ask ten different financial advisors what your portfolio should look like, and most of them will eventually point to the same two ingredients: stocks and bonds. Everything else — real estate, commodities, cash, crypto — tends to get layered around this core pairing rather than replacing it.

The reason these two asset classes anchor so much of modern investing isn’t complicated: stocks and bonds tend to behave differently from each other, especially when markets get rough, which means owning both can smooth out the ride without giving up too much long-term growth. But “own both” only gets you so far — the real decisions are how much of each, when, and why. Before diving in, if terms like “yield” or “dividend” still feel slippery, it might help to first skim our broader financial planning tips, since this comparison builds on that foundation rather than repeating it.

Section 01

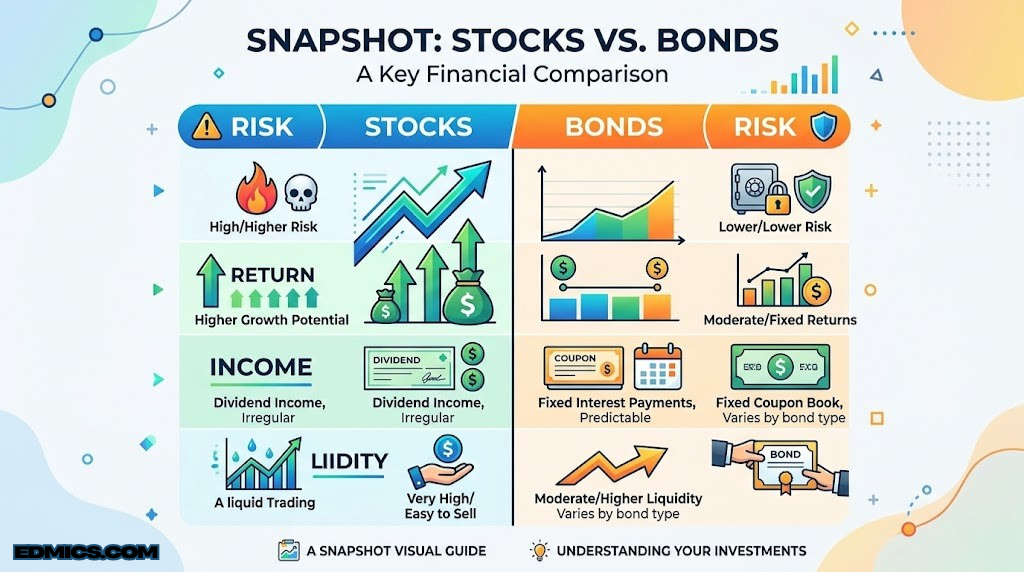

Quick Comparison: Stocks vs Bonds

At the most basic level, a stock represents partial ownership in a company, while a bond represents a loan you’ve made to a company or government, which pays you interest until it’s repaid. Everything else in this guide is really just an elaboration on that one sentence — but the elaboration matters, because “ownership” and “lending” behave very differently when the economy wobbles.

| Characteristic | Stocks | Bonds |

|---|---|---|

| What you actually own | A share of a company’s future profits | An IOU promising interest plus repayment |

| How you get paid | Price appreciation, sometimes dividends | Regular coupon payments, plus face value at maturity |

| Typical volatility | High — can swing sharply year to year | Lower, though not zero |

| Growth potential | Highest among mainstream asset classes | Modest, more predictable |

| Income reliability | Variable; dividends can be cut | Fixed schedule, barring default |

| Worst-case scenario | Company fails, shares can go to zero | Issuer defaults, but often partial recovery |

| Time horizon fit | Long-term goals (years to decades) | Shorter-term or income-focused goals |

The simplest framing: stocks are how money grows over time, and bonds are how it stays steady along the way. Most long-term portfolios use some blend of both rather than betting everything on one side — the rest of this guide explains why, and how to think about your own blend.

Section 02

What Are Stocks? Owning a Piece of a Company

When you buy a share of stock, you’re buying a small slice of ownership in a real business — its factories, its brand, its future earnings, and crucially, its risks. If the company grows its profits, the value of your slice tends to grow too. If the company struggles, your slice can lose value right alongside it. There’s no fixed schedule, no guaranteed payout, and no ceiling on how high or low things can go.

Two Ways Stocks Can Pay You

The first is price appreciation: you buy a share at one price and, hopefully, sell it later at a higher one. The second is dividends — periodic cash payments some companies choose to distribute from their profits, separate from any change in share price. Not every company pays dividends; many growth-focused companies reinvest everything back into the business instead. For investors who specifically want income from their stock holdings, our roundup of the highest dividend-paying stocks is a useful reference for how that side of the equity world looks in practice.

What Makes Stock Ownership Different

Unlike a bond, a stock has no maturity date and no promise of repayment. You’re not owed anything — you simply own a piece of whatever the company becomes. That’s the source of both stocks’ biggest upside (unlimited growth potential if the company thrives) and their biggest risk (shareholders are typically last in line if a company goes bankrupt, after bondholders and other creditors are paid).

Common Stocks vs Preferred Stocks

Most individual investors own “common stock,” which comes with voting rights but no guaranteed dividend. “Preferred stock” sits in between common stock and bonds — it typically pays a fixed dividend (more bond-like) but usually doesn’t come with voting rights, and still ranks behind bondholders in a bankruptcy. You’ll encounter preferred shares less often as a beginner, but it’s worth knowing the category exists.

Desk Pick

Financial Calculator for Growth Projections

Running quick “what if I invested this much for this many years” math is far easier with a dedicated financial calculator than fumbling through a phone app mid-conversation.

Check Price on AmazonSection 03

What Are Bonds? Lending Money for Steady Income

A bond is essentially a loan in reverse: instead of borrowing money from a bank, a government or company borrows money from you (and thousands of other investors) by issuing bonds. In exchange, the issuer promises to pay you interest — called the “coupon” — on a regular schedule, and to return the original amount you lent (the “face value” or “principal”) when the bond matures.

The Three Numbers That Define a Bond

Every bond can be described by three core figures: its face value (what you’ll be repaid at maturity), its coupon rate (the interest rate it pays, usually as a percentage of face value), and its maturity date (when the loan comes due). A bond with a face value of $1,000, a coupon rate of 4%, and a 10-year maturity will pay you $40 a year for ten years, then return your original $1,000.

Who Issues Bonds, and Why It Matters

Governments issue bonds to fund everything from infrastructure to general operating budgets — this is part of how national income gets allocated and how public spending is financed without raising taxes immediately. Corporations issue bonds to fund expansion, refinance debt, or manage cash flow without diluting ownership by issuing more stock. Generally speaking, government bonds from stable countries are considered among the safest investments available, while corporate bonds carry varying degrees of additional risk depending on the issuing company’s financial health — which is exactly the kind of thing you’d assess by reading a company’s balance sheet.

Why Bond Prices Move at All

If a bond pays a fixed amount no matter what, why would its price change before maturity? Because bonds trade on a secondary market, and their price adjusts so that the effective yield stays competitive with current interest rates. If new bonds start being issued at higher rates, existing bonds with lower fixed coupons become less attractive and their price drops to compensate — and vice versa when rates fall. We’ll come back to this relationship in more detail later, since it’s one of the most misunderstood parts of bond investing.

Section 04

How Returns Work: Capital Gains, Dividends & Coupons

“Return” means something slightly different depending on which asset you’re holding, and mixing up the two can lead to apples-to-oranges comparisons that make one asset look better or worse than it really is.

Stock Returns: Mostly About the Future

A stock’s return is driven primarily by changing expectations about a company’s future profits. If investors collectively decide a company will earn more than previously expected, the share price tends to rise — even before those higher profits actually show up. This forward-looking pricing is why stock markets can feel disconnected from current headlines: prices are constantly trying to anticipate what comes next, not just react to what already happened. Dividends, when paid, add an additional layer of return on top of any price movement, and reinvesting those dividends (buying more shares with the cash instead of spending it) is one of the most powerful long-term compounding tools available to ordinary investors — the same compounding logic explored in our piece on why earning interest on interest matters so much.

Bond Returns: Mostly Locked In Upfront

A bond’s return, by contrast, is largely determined the moment you buy it — assuming you hold it to maturity and the issuer doesn’t default, you know almost exactly what you’ll receive and when. The coupon payments arrive on schedule, and the face value is returned at maturity. The main variable is what happens if you sell before maturity, at which point the price you get depends on prevailing interest rates at that moment, as described earlier.

Total Return vs Yield

For both assets, it’s worth distinguishing between “yield” (the income a holding generates, expressed as a percentage) and “total return” (income plus any price change, combined). A bond’s yield is fairly stable; a stock’s dividend yield is also relatively stable, but total return for a stock is dominated by price movement, which can swing wildly in either direction over short periods. When comparing investment options — including funds that bundle many stocks or bonds together — our comparison of index funds vs mutual funds walks through how these return figures get reported in practice.

Desk Pick

Desk Organizer for Statements & Paperwork

Brokerage statements, 1099 forms, and bond confirmations pile up fast — a simple tiered organizer keeps this year’s documents from drowning your desk.

Check Price on AmazonSection 05

Risk & Volatility: Why Stocks Swing and Bonds (Mostly) Don’t

If you’ve ever watched a stock portfolio drop several percent in a single afternoon and then recover just as quickly the next week, you’ve experienced volatility firsthand. Bonds can move too — sometimes substantially — but the day-to-day swings are typically much smaller, and the path to maturity is far more predictable.

Illustrative only — not actual market data

What “Volatility” Actually Measures

Volatility describes how much an asset’s price moves around over a given period, regardless of direction. A highly volatile asset can post a great year and a terrible year back to back; a low-volatility asset tends to move in smaller, steadier increments. Stocks are volatile because their value depends on collective expectations about an uncertain future — expectations that can shift quickly based on earnings reports, economic data, or even shifts in investor sentiment driven by basic supply and demand dynamics playing out in real time across millions of buy and sell orders.

Why Bonds Are Calmer (Most of the Time)

A bond’s cash flows are largely fixed in advance, so there’s less for investors to argue about — the main thing that changes a bond’s price is shifting interest rate expectations, which tend to move more gradually than corporate earnings surprises. That said, “calmer” doesn’t mean “risk-free.” Long-term bonds, in particular, can experience meaningful price swings when interest rate expectations shift suddenly, and certain categories of bonds (covered in a later section) can be just as volatile as stocks in extreme circumstances.

Volatility Isn’t Only “Bad”

It’s tempting to treat volatility purely as a risk to be minimized, but volatility is also the mechanism through which stocks generate their higher long-term returns — investors demand a higher expected return for tolerating more uncertainty, a relationship sometimes called the risk-return tradeoff. The practical takeaway isn’t “avoid volatility” but “make sure the volatile portion of your portfolio is money you won’t need on short notice.”

Section 06

Performance Over Time: Growth vs Stability

Over long stretches of time, broad stock markets have historically delivered higher average returns than broad bond markets — this is the core justification for holding stocks at all despite their volatility. But “higher on average” hides a lot of texture worth understanding before you build a plan around it.

Averages Hide the Bumpy Path

A long-term average return doesn’t mean returns arrive smoothly, year after year, at that average rate. In reality, stock returns are lumpy: some years deliver outsized gains, others deliver outsized losses, and the long-term average emerges only after enough of these ups and downs have played out. This is precisely why time horizon matters so much — the longer your money stays invested, the more chances it has for strong years to offset weak ones.

Bonds Provide the “Floor”

Bonds rarely deliver the eye-catching returns stocks can, but they also rarely deliver the gut-wrenching losses. Their role in a portfolio is often less about maximizing growth and more about providing a more predictable floor — money that’s likely to be roughly where you expect it when you need it, which matters enormously for goals with a fixed deadline.

Inflation Changes the Comparison

Any discussion of “returns” should account for inflation — a return that doesn’t outpace rising prices isn’t really growing your purchasing power, even if the number on your statement is going up. This is a particularly important consideration for bonds, since their fixed payments are worth less in real terms if inflation runs hot during the bond’s life. When thinking about long-term goals like how much to save for retirement, this inflation-adjusted view of returns matters far more than the headline numbers on either asset class.

For a broader sense of how stocks and bonds compare to other places people put money — savings accounts, real estate, or alternative assets — our roundup of where money has historically grown provides useful context for where this pairing fits in the bigger picture.

Desk Pick

Noise-Cancelling Headphones for Deep Research

Reading through fund prospectuses or annual reports takes focus — a solid pair of noise-cancelling headphones makes that kind of reading a lot less interruptible.

Check Price on AmazonSection 07

Stock-Specific Risks You Should Understand

“Stocks are risky” is true but unhelpfully vague. Several distinct types of risk get bundled into that one word, and understanding each one separately makes it much easier to manage them.

Company-Specific Risk

This is the risk that something goes wrong with one particular business — poor management decisions, a failed product launch, a scandal, or outright bankruptcy. This is the risk that diversification (owning many different stocks rather than just one or two) is specifically designed to reduce. If you’ve never read a company’s financial statements before deciding whether to invest, our guide to reading a balance sheet is a good starting point for spotting warning signs.

Market Risk

Even a well-run company’s stock can fall simply because the overall market is falling — driven by broad economic concerns, interest rate changes, or shifts in investor sentiment that have nothing to do with that specific company’s performance. Diversification across companies doesn’t eliminate this risk, since it affects the market broadly; this is part of why bonds, which often respond differently to the same economic conditions, play a complementary role.

Concentration Risk

This is the risk of having too much tied up in one company, one sector, or one country. It’s easy to drift into concentration without noticing — for example, owning your employer’s stock through a retirement plan in addition to already depending on that employer for your salary doubles up your exposure to that single company’s fortunes.

Behavioral Risk

Perhaps the least discussed but most damaging risk isn’t about the market at all — it’s about how investors react to it. Selling during a downturn (locking in losses) and buying during euphoric peaks (locking in high prices) is a well-documented pattern that erodes returns far more than most “market” risks do. Having a plan in advance, and a basic decision-making framework for sticking to it, is one of the most underrated risk-management tools available — far more accessible than anything requiring market-timing skill.

Section 08

Bond-Specific Risks: Interest Rates, Credit & Inflation

Bonds are often described as “safe,” and relative to stocks, they generally are — but “safer” isn’t the same as “risk-free.” Three risks in particular are worth understanding before assuming a bond allocation is automatically a low-risk decision.

Interest Rate Risk

This is the risk that bond prices fall when interest rates rise, since newly issued bonds with higher rates make existing lower-rate bonds less attractive by comparison. The longer a bond’s time to maturity, the more sensitive its price tends to be to rate changes — a bond maturing in twenty years will typically swing more in price than one maturing in two years, for the same change in rates. If you’re holding a bond to maturity, these price swings don’t affect what you’ll ultimately receive, but they very much affect what you’d get if you needed to sell early.

Credit Risk (Default Risk)

This is the risk that the issuer can’t make its promised payments — whether that’s a struggling company or, in rarer cases, a government facing fiscal distress. Bonds from issuers considered less likely to repay typically have to offer higher coupon rates to attract buyers, which is why “higher-yielding” bonds are often a signal of higher risk, not just a better deal. Assessing this risk for corporate bonds involves much the same analysis as assessing a company’s stock — understanding its income statement and overall financial health.

Inflation Risk

Because most bonds pay a fixed amount, unexpected inflation erodes the real value of those payments. A bond paying 3% annually feels very different if inflation is running at 1% versus 5% — the nominal payment is identical, but its purchasing power isn’t. This is one reason cash-heavy or bond-heavy portfolios can struggle to keep pace with rising costs over long periods, even while technically avoiding stock market losses.

Reinvestment Risk

When a bond matures or pays a coupon, that money needs to go somewhere — and if interest rates have fallen since you originally bought the bond, reinvesting at the new, lower rates means lower future income than you were previously receiving. This is the flip side of interest rate risk, and it’s a particular concern for investors relying on bond income to cover ongoing expenses.

When Stocks Tend to Make Sense

- Your goal is years or decades away

- You can emotionally tolerate seeing the value drop temporarily

- You’re building long-term wealth, not funding near-term expenses

When Bonds Tend to Make Sense

- Your goal has a fairly fixed, nearer-term date

- You want predictable income on a known schedule

- You’re balancing out a stock-heavy portfolio’s swings

Section 09

Taxes on Stocks vs Bonds

How an investment performs on paper and how it performs after taxes can be two very different stories, and stocks and bonds are taxed in meaningfully different ways.

How Stock Gains Are Taxed

When you sell a stock for more than you paid, the profit is a capital gain. How long you held the stock before selling typically determines the tax rate: gains on assets held longer than a year (long-term gains) are usually taxed at lower rates than gains on assets held for a year or less (short-term gains), which are often taxed the same as ordinary income. Dividends add another layer — “qualified” dividends from many domestic companies are often taxed at the same favorable rates as long-term capital gains, while other dividends are taxed as ordinary income.

How Bond Income Is Taxed

Interest income from most bonds — corporate bonds in particular — is generally taxed as ordinary income, at your regular income tax rate, regardless of how long you’ve held the bond. This is one reason bonds are sometimes described as “tax-inefficient” compared to stocks held for the long term. There’s a notable exception: interest from certain government bonds, particularly municipal bonds in some jurisdictions, can be exempt from certain levels of taxation, which is part of why those bonds often carry lower stated yields — the tax benefit is baked into the comparison.

The Account Matters as Much as the Asset

Where you hold an investment can matter just as much as what the investment is. Many countries offer tax-advantaged retirement or savings accounts that defer or eliminate taxes on investment growth, which changes the calculus considerably — a bond’s “tax-inefficient” interest income looks very different when it’s not generating an annual tax bill at all. This is part of why “asset location” (which accounts hold which assets) is a real strategy that financial planners discuss alongside “asset allocation.”

None of this is a substitute for working with a tax professional or quality tax software on your specific situation — if you’re comparing tools to handle the filing side once tax season arrives, our breakdowns of TurboTax vs H&R Block and TurboTax vs FreeTaxUSA cover how each handles investment income reporting specifically.

Desk Pick

Leather Padfolio for Tax Season Documents

Between 1099s, cost-basis reports, and brokerage summaries, tax season generates a stack of paper — a padfolio keeps it organized and presentable if you’re meeting with a preparer.

Check Price on AmazonSection 10

Liquidity & How to Actually Buy Each

“Liquidity” describes how quickly and easily you can convert an investment back into cash without significantly affecting its price. Both stocks and bonds are generally liquid compared to assets like real estate, but the experience of buying and selling each differs in practical ways.

Buying Stocks

Individual stocks trade on public exchanges throughout the trading day, and for widely-traded companies, buying or selling a typical retail-sized position is usually fast and has minimal impact on the price. Most investors buy stocks through a brokerage account, and the process is largely the same regardless of which company’s shares you’re buying.

Buying Bonds

Individual bonds work differently. Many bonds trade less frequently than popular stocks, and the gap between the price a buyer is willing to pay and a seller is willing to accept (the “bid-ask spread”) can be wider, particularly for smaller or less commonly traded issues. Government bonds from major economies tend to be highly liquid; smaller corporate bond issues, less so. For many individual investors, this is a major reason to access bonds through funds rather than buying individual bonds directly.

Choosing Where to Hold Your Investments

Whichever assets you choose, you’ll need a brokerage account to hold them, and the differences between brokerages — fees, available research tools, account types, and customer service — can matter more than people expect. If you haven’t settled on a brokerage yet, our side-by-side comparison of Fidelity and Charles Schwab covers two of the most commonly used options for both stock and bond investing. More broadly, our guide to where to invest money covers how brokerage accounts fit alongside other places your money might go.

Settlement Times & Why They Matter

When you sell an investment, there’s often a short delay — called the “settlement period” — before the cash is fully available to withdraw or reinvest elsewhere, even though the trade itself executes almost instantly. This is rarely a major issue for long-term investors, but it’s worth knowing about if you’re planning to use proceeds from a sale for something time-sensitive, like a down payment.

Desk Pick

Lightweight Tablet for Market Research

Checking your brokerage app, reading a prospectus, or comparing fund fact sheets is easier on a larger screen — a compact tablet hits a nice middle ground between phone and laptop.

Check Price on AmazonSection 11

Building a Portfolio: Asset Allocation Between Stocks and Bonds

“Asset allocation” is simply the term for how your money is divided across different types of investments — and for most portfolios, the stock-versus-bond split is the single biggest decision in that allocation, more influential than which specific stocks or bonds you pick.

Why the Split Matters More Than the Picks

Research on portfolio outcomes consistently points to asset allocation — the broad mix between asset classes — as a bigger driver of long-term results than individual security selection within those classes. In practical terms: deciding “I’ll hold 70% stocks and 30% bonds” matters more to your eventual outcome than agonizing over exactly which stocks make up that 70%.

Common Starting Frameworks

Several rules of thumb exist for setting an initial stock-bond split, often based on age or time horizon — the general idea being that more time until you need the money supports a higher stock allocation, since there’s more time to recover from downturns. These rules of thumb are starting points, not laws of physics; your actual risk tolerance, other assets (like a pension or property), and specific goals all matter too. This is really a specific application of the broader process of organizing from goals to a working structure — you start with what you’re trying to achieve, then build the structure (your allocation) that supports it.

Rebalancing: The Maintenance Step Most People Skip

Over time, if stocks grow faster than bonds (as they often do), your portfolio’s actual allocation will drift away from your target — a 70/30 split can quietly become 80/20 after a strong few years for stocks, without you doing anything. Rebalancing means periodically buying or selling to bring the mix back toward your target, which has the side effect of systematically taking some profit from whatever’s grown the most and adding to whatever’s lagged — a disciplined version of “buy low, sell high” that doesn’t require predicting anything.

Allocation Is Part of a Bigger Plan

Your stock-bond split doesn’t exist in isolation — it’s one piece of a broader approach to wealth management that also includes how much you’re saving, what accounts you’re using, and what you’re working toward. If you’re still working out the budgeting side of the equation — how much surplus you actually have to allocate in the first place — our guide on what to prioritize when creating a budget is a useful companion to this one.

Desk Pick

Fireproof Safe for Investment Records

Even with everything online, year-end statements, cost-basis records, and the occasional paper bond certificate deserve a fireproof, waterproof home.

Check Price on AmazonSection 12

Beyond Stocks and Bonds: ETFs, Mutual Funds & Other Vehicles

For most people, “investing in stocks” and “investing in bonds” doesn’t mean picking individual companies or individual bonds one at a time — it means buying funds that hold many of them at once, bundled into a single, easily-traded investment.

Funds as the Practical Default

A fund that holds hundreds of stocks gives you instant diversification that would take significant time and money to build by purchasing individual shares one at a time. The same logic applies to bonds: a bond fund holds many individual bonds with staggered maturities, smoothing out some of the liquidity and reinvestment concerns that come with holding individual bonds directly. Our comparison of ETFs vs mutual funds covers the practical differences between the two most common fund structures — trading flexibility, minimum investments, and how each is typically taxed.

A Bond Fund Isn’t Quite the Same as a Bond

One subtlety worth flagging: an individual bond held to maturity has a defined endpoint and a known return (absent default). A bond fund, by contrast, continuously buys and sells bonds and has no maturity date itself — its value will fluctuate with interest rates indefinitely, for as long as you hold it. This doesn’t make bond funds worse, but it does mean the “just hold it to maturity and you’re guaranteed your money back” logic that applies to individual bonds doesn’t translate directly to bond funds.

Where Other Assets Fit In

Stocks and bonds form the core of most portfolios, but they’re not the only options. Real estate, for instance, behaves differently from both and is covered in depth in our guide to real estate investing. Newer asset classes like cryptocurrency occupy yet another risk category entirely — often more volatile than stocks, with a much shorter track record, and requiring different infrastructure to hold securely, which is where resources like our guide to hardware wallets for crypto come in for anyone exploring that space. None of these replace a stock-and-bond foundation, but they’re worth knowing exist as you think about diversification more broadly.

Desk Pick

Hardware Wallet for Holding Crypto Securely

If you’re branching into cryptocurrency alongside your stock and bond holdings, a hardware wallet keeps those assets off exchange servers and under your own control.

Check Price on AmazonSection 13

Matching the Right Mix to Your Life Stage and Goals

There’s no single “correct” stocks-to-bonds ratio — the right mix depends on what the money is for and when you’ll need it. Rather than a one-size-fits-all number, it helps to think in terms of a few common scenarios.

Long Runway, Long-Term Growth

If you’re investing for a goal that’s decades away — retirement being the classic example for someone early or mid-career — a higher stock allocation has historically made sense, because there’s enough time for the market’s ups and downs to average out, and the higher growth potential compounds meaningfully over that timeframe.

Approaching a Goal With a Real Deadline

As a specific goal gets closer — a house down payment in two years, a child’s education starting in five — the calculus shifts. Money you’ll need on a specific timeline is money that can’t afford a poorly-timed market downturn right before you need it, which is exactly the scenario where a higher bond (or cash) allocation for that specific goal starts to make more sense, even if your overall portfolio skews toward stocks.

Already Living Off Your Portfolio

For someone already retired and drawing income from their investments, the priorities shift again: predictable income and capital preservation often become more important than maximizing growth, though most retirees still benefit from holding some stocks to combat inflation over a retirement that could last decades.

Know Your Numbers Before You Set Your Mix

None of this works without a clear picture of your actual cash flow — how much you’re spending, saving, and have available to invest in the first place. Personal finance tracking tools make this far less tedious than it used to be; our comparisons of Mint vs YNAB and Personal Capital vs Mint cover popular options for getting that picture clear before you start fine-tuning an allocation. And if one of your goals involves funding education — your own or a family member’s — resources like our overview of accredited online business degrees can help you size up what that specific goal might actually cost, which then feeds back into how you’d plan around it.

Section 14

Common Mistakes Investors Make With Stocks and Bonds

Most of the costly mistakes in this space aren’t about picking the wrong stock or the wrong bond — they’re about how people think about the relationship between the two.

Treating It as an All-or-Nothing Choice

“Stocks vs bonds” can sound like a competition with a winner, but for most investors it’s not a competition at all — it’s a blend. Going 100% into whichever asset performed better recently is a common reaction to short-term news, and it tends to mean buying high (chasing what just went up) and selling low (abandoning what just went down) — the opposite of what you’d actually want.

Confusing “Lower Volatility” With “No Risk”

As covered earlier, bonds carry their own risks — interest rate risk, credit risk, and inflation risk among them. Treating a bond-heavy portfolio as automatically “safe” without considering these factors, especially over long time horizons, is a subtle but meaningful mistake.

Never Reviewing the Mix

Setting an allocation once and never revisiting it means your actual risk level can drift significantly over time, as covered in the rebalancing discussion earlier. Periodically reviewing your portfolio is, in a sense, a personal version of the same logic behind why businesses conduct audits — not because anything is necessarily wrong, but because regular review is what catches drift before it becomes a problem. Our explainer on the purposes and advantages of an audit makes this case in a business context, but the underlying logic applies just as well to a personal portfolio nobody has looked at in years.

Reacting Instead of Deciding

Selling during a downturn because it’s frightening, or buying something because a headline made it sound exciting, are both examples of reacting rather than deciding. A more durable approach starts with clearly understanding the elements of the decision situation — what you’re actually trying to achieve, what your real constraints are — before acting, and following a consistent decision-taking process rather than a gut reaction to the news of the day.

Ignoring Costs

Fees on funds, trading costs, and tax inefficiencies all quietly compound over time, the same way returns do — just in the opposite direction. A small difference in ongoing costs can add up to a meaningful difference in outcomes over a multi-decade investing timeline, which is part of why comparing fund structures (as covered earlier) is worth the relatively small effort it takes.

Section 15

Frequently Asked Questions

What’s the main difference between a stock and a bond?

A stock represents partial ownership in a company, with returns driven by changes in the company’s value and, sometimes, dividends. A bond represents a loan you’ve made to a company or government, which pays you fixed interest on a schedule and returns your principal at maturity. Ownership versus lending is the core distinction everything else flows from.

Are bonds always safer than stocks?

Bonds are generally less volatile than stocks day to day, but “safer” depends on what risk you’re measuring. Bonds carry their own risks, including interest rate risk, credit risk, and inflation risk. Over very long periods, a bond-heavy portfolio can also underperform inflation, which is its own form of risk even if the account balance never drops sharply.

Can you lose money investing in bonds?

Yes. If you sell a bond before maturity, its price may have fallen due to rising interest rates, resulting in a loss. If an issuer defaults, you may not receive full interest payments or principal back. And even bonds held to maturity without default can lose purchasing power if inflation outpaces the fixed interest rate over the bond’s life.

How much of my portfolio should be in stocks versus bonds?

There’s no universal answer — it depends on your time horizon, goals, and comfort with seeing your balance fluctuate. Common starting frameworks often tie the split to age or years until the money is needed, with longer horizons supporting higher stock allocations. These are starting points for a conversation, not a formula that fits everyone exactly.

Do bonds pay dividends like stocks do?

No — bonds pay “coupon” interest on a fixed schedule rather than dividends. Dividends are a discretionary distribution some companies choose to pay from profits and can be reduced or eliminated. Bond coupon payments are a contractual obligation tied to the loan you’ve made, with a defined rate and schedule set when the bond was issued.

What happens to bond prices when interest rates rise?

Existing bond prices typically fall when interest rates rise, because newly issued bonds offering higher rates make older, lower-rate bonds less attractive by comparison. Longer-maturity bonds tend to be more sensitive to this effect than shorter-maturity bonds. If you hold a bond to maturity, this price movement doesn’t change what you’ll ultimately be repaid.

Are stocks or bonds better for retirement savings?

Most retirement portfolios use both, with the mix shifting over time. Earlier in a career, a higher stock allocation is common to capture long-term growth. As retirement approaches and especially during retirement, a larger bond allocation often helps provide more predictable income and reduce the impact of a poorly-timed downturn on money you’re actively drawing from.

How are stock and bond returns taxed differently?

Stock gains held longer than a year, and many dividends, are often taxed at favorable long-term capital gains rates. Bond interest is generally taxed as ordinary income at your regular rate, regardless of how long you’ve held the bond, with some exceptions for certain government bonds. The account type you hold either in — taxable versus tax-advantaged — also significantly affects the outcome.

What’s the difference between owning a bond directly and owning a bond fund?

An individual bond held to maturity has a defined endpoint and a known return absent default. A bond fund holds many bonds, has no maturity date of its own, and continuously buys and sells, so its value fluctuates with interest rates for as long as you hold it. Funds offer diversification and convenience, but without the “guaranteed-at-maturity” structure of a single bond.

Do stocks or bonds tend to perform better during a recession?

Bonds, particularly higher-quality government bonds, have historically tended to hold up better than stocks during economic downturns, partly because investors often seek safer, income-generating assets during uncertain periods. This isn’t guaranteed in every downturn, and certain categories of bonds can behave more like stocks during severe credit stress, but the general pattern is part of why bonds are often described as a portfolio stabilizer.

Should beginners start with stocks, bonds, or both?

Most beginners are better served starting with a diversified mix rather than picking one extreme, often through a simple fund that already blends stocks and bonds in a set ratio. This avoids the common trap of trying to perfectly time which asset to “start with” and instead gets you invested in a reasonable, diversified way while you continue learning — with adjustments coming later as your goals and knowledge develop.

Section 16 · Final Takeaway

Stocks vs Bonds: The Bottom Line

Stocks and bonds aren’t rivals competing for a single spot in your portfolio — they’re tools that do different jobs. Stocks are the engine that drives long-term growth, with volatility as the price of admission. Bonds are the ballast that keeps the ride steadier and provides more predictable income, with more modest growth as the tradeoff.

Stocks

Best suited to money with a long runway, where you can ride out volatility in exchange for higher long-term growth potential. The longer your time horizon, the more this volatility tends to wash out.

Bonds

Best suited to money you’ll need on a more specific timeline, or to dampen the swings of a stock-heavy portfolio. Predictability is the point, even if growth is more modest.

If you take away one thing from this guide, let it be this: the “right” mix isn’t a fixed number you find once and forget — it’s a reflection of your goals, timeline, and comfort with risk, all of which can shift over time. And if you’re a business owner thinking through this for surplus cash sitting in the company’s accounts, the same logic applies, just layered on top of however you’re already tracking the books in QuickBooks or Xero.